First-Time Homebuyer’s Roadmap for 2026: Overcoming Affordability Challenges in Edmonton

Is 2026 the Year You Finally Enter the Edmonton Housing Market?

As we settle into 2026, the Edmonton real estate landscape is shifting. While affordability remains a top concern for many first-time buyers, market conditions are showing signs of what we call the “mortgage sweet spot.” With interest rates stabilizing and becoming more predictable compared to the volatility of previous years, opportunities are opening up for those who have a strategic plan.

However, buying your first home in neighborhoods like Oliver, Strathcona, or the growing suburbs requires more than just browsing listings. It demands a roadmap tailored to overcoming today’s specific financial hurdles. Whether you are tired of renting or looking to build long-term wealth, navigating high prices and qualifying rules requires expert guidance. As your dedicated Edmonton mortgage broker, I am here to help you map out a journey that leads to a stress-free possession day.

Leveraging Assistance Programs and Smart Financing

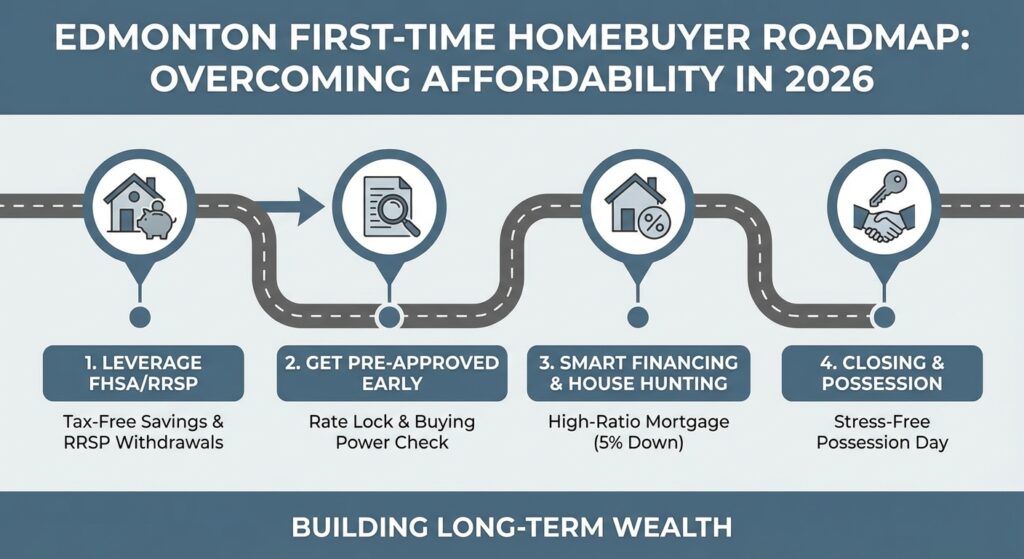

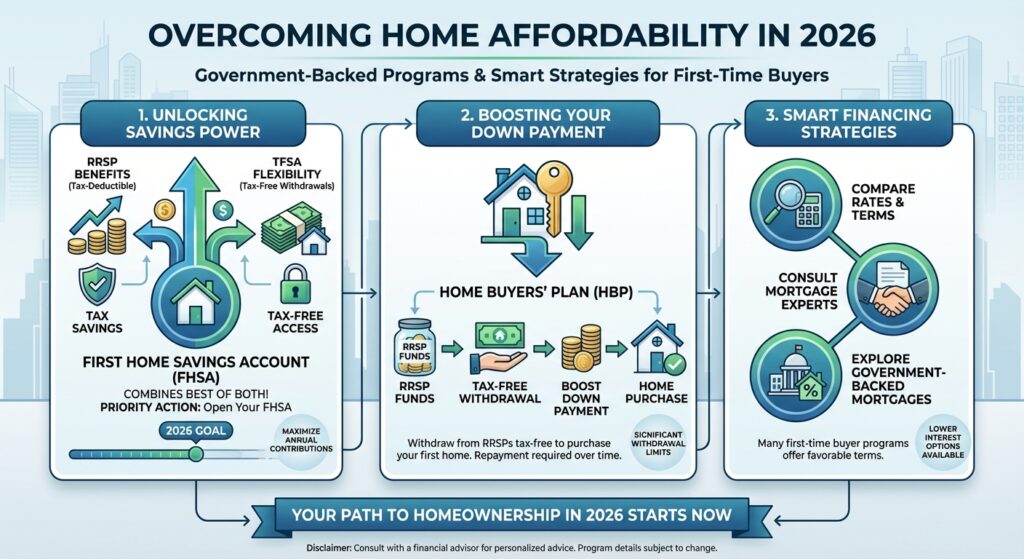

Overcoming affordability challenges in 2026 starts with utilizing government-backed assistance programs designed specifically for buyers like you. If you haven’t yet opened a First Home Savings Account (FHSA), this should be your priority; it combines the tax-deductibility of an RRSP with the tax-free withdrawals of a TFSA. Additionally, the Home Buyers’ Plan (HBP) allows you to withdraw from your RRSPs tax-free to boost your down payment.

Beyond saving, smart financing is critical. Many first-time buyers assume they need a 20% down payment, but in Edmonton, you can purchase a home for as little as 5% down on the first $500,000 through a high-ratio mortgage backed by default insurance (CMHC, Sagen, or Canada Guaranty). While this adds an insurance premium to your mortgage, it allows you to stop renting sooner and start building equity.

- Get Pre-Approved Early: In a competitive market, a pre-approval locks in your rate for up to 120 days, protecting you from sudden rate hikes while you shop.

- Understand Your Buying Power: We calculate your Total Debt Service (TDS) ratios to ensure you aren’t just approved, but comfortable with your monthly payments.

| Mortgage Feature | Big Bank Offer | Jason Scott (Broker) Offer | Potential Impact |

|---|---|---|---|

| Interest Rate (5-Year Fixed) | 6.09% (Posted Rate) | 3.89% (Discounted Rate) | Significant monthly savings |

| Lender Options | 1 (Their own products) | 20+ Lenders | More choices, better fit |

| Pre-Approval Hold | Varies (Often 90 days) | Up to 120 Days | Longer rate protection |

| Advice Type | Sales-driven | Unbiased & Independent | Strategies tailored to you |

The Broker Advantage: Why Independent Advice Matters

One of the biggest mistakes first-time buyers make is walking into their local bank branch and accepting the first rate offered. As an independent broker with TMG The Mortgage Group, I work for you, not the banks. This means I can shop your mortgage to over 20 different lenders to find not just the best rate, but the best terms.

For example, some low-rate mortgages come with restrictive “bonafide sales clauses” that prevent you from breaking the mortgage unless you sell the property. This can be a trap if you need to refinance or move unexpectedly. My goal is to educate you on these fine print details so you can make a confident decision. Whether you are looking for a stable fixed rate or a variable product with potential for savings, we will customize a strategy that aligns with your financial goals for 2026 and beyond.

Q1: What is the minimum down payment for a home in Edmonton in 2026?

For homes with a purchase price of $500,000 or less, the minimum down payment is 5%. For homes between $500,000 and $999,999, it is 5% on the first $500k and 10% on the remainder.

Q2: How does a mortgage pre-approval help me?

A pre-approval confirms your borrowing limit and locks in an interest rate for up to 120 days. This protects you from rate increases and shows sellers you are a serious, qualified buyer.

Q3: Should I choose a fixed or variable rate as a first-time buyer?

It depends on your risk tolerance and budget. Fixed rates offer stability with consistent payments, while variable rates can save money if prime rates drop but come with fluctuating costs.

Q4: What are closing costs, and how much should I budget?

Closing costs cover legal fees, land title transfer, and adjustments. You should generally budget between 1.5% and 2% of the purchase price, in addition to your down payment.

Q5: Do I pay a fee to use a mortgage broker?

In most cases, no. For qualified borrowers with good credit, my services are free because the lender pays a finder’s fee once your mortgage is funded.

{kind=link}

{kind=link}