Why 2026 is the Prime Time to Leverage Your Edmonton Home’s Equity

As we navigate the Edmonton real estate market in 2026, many homeowners are finding themselves in a unique position of strength. Property values in neighborhoods like Strathcona and Oliver have remained resilient, and for those who have owned their homes for several years, the accumulated equity represents a significant financial tool. Cash-out refinancing allows you to access this wealth by replacing your current mortgage with a new, larger one, and taking the difference in cash.

Unlike a standard renewal, a refinance involves breaking your existing term to access funds up to 80% of your home’s appraised value. Whether you are looking to fund a major renovation, purchase an investment property in YEG, or consolidate high-interest debt, refinancing can be a strategic move. As an expert Edmonton mortgage broker, I help clients navigate the changing lending landscape to ensure that accessing your equity aligns with your long-term financial freedom.

Top Strategies: Renovations, Investing, and Debt Consolidation

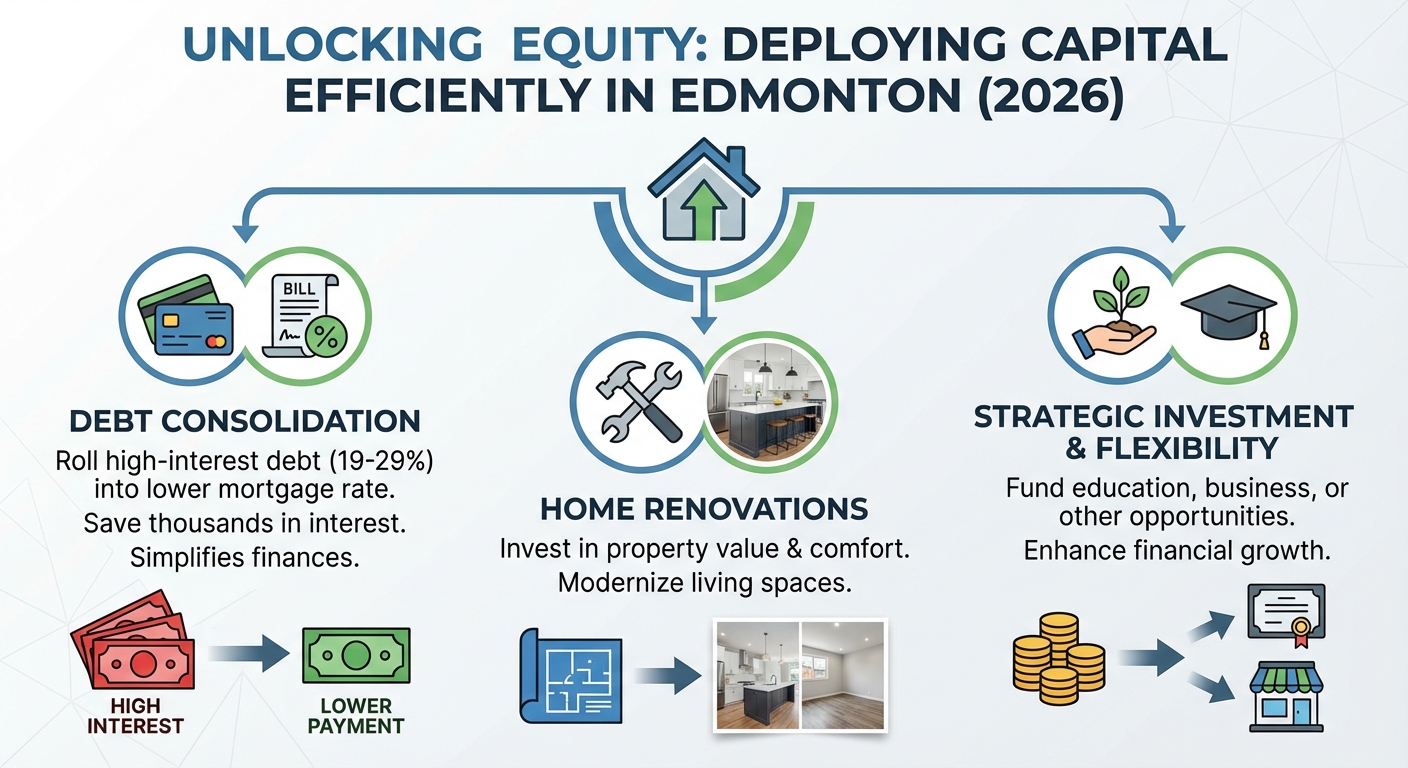

Unlocking equity is about more than just having extra cash; it is about deploying capital efficiently. Here are the three most common and effective ways Edmontonians are utilizing cash-out refinancing in 2026:

- Debt Consolidation: With credit card interest rates often hovering around 19-29%, rolling that debt into a mortgage rate (typically much lower) can save thousands in interest payments. This improves monthly cash flow and simplifies finances into one payment.

- Home Renovations: Investing in your property—whether it’s a kitchen upgrade or a basement suite—can increase your home’s value. In Edmonton’s competitive market, modernizing your home is a smart way to build further equity.

- Real Estate Investment: Using equity as a down payment for a rental property is a classic wealth-building strategy. With the right guidance, you can leverage your current home to expand your portfolio.

However, it is crucial to calculate the costs. Refinancing may trigger a prepayment penalty (3 months’ interest or the Interest Rate Differential). As your broker, I calculate these costs against your potential savings to ensure the math works in your favor.

| Debt Type | Interest Rate (Approx.) | Monthly Payment | Total Interest (5 Years) |

|---|---|---|---|

| Credit Cards ($30k balance) | 19.99% | $900 (Min. Payment) | ~$25,000+ |

| Personal Loan ($20k balance) | 9.00% | $450 | ~$4,500 |

| Refinanced Mortgage ($50k added) | ~4.50% | ~$275 | ~$10,500 (over longer term) |

Navigating the Refinance Process with Jason Scott

Refinancing is not a one-size-fits-all solution. Lending rules in Canada are strict, specifically the stress test and the 80% Loan-to-Value (LTV) limit. This means you must maintain at least 20% equity in your home after the refinance. Working with an independent broker like myself, Jason Scott, ensures you have access to over 20 lenders, not just the big banks. This allows us to shop for the best rates and terms that suit your specific financial profile.

My process is transparent and client-focused. We start by reviewing your current mortgage penalty and comparing it against the savings or returns you expect from refinancing. If you are looking to refinance your mortgage, I handle the heavy lifting—from arranging the appraisal to coordinating with lawyers—making the experience stress-free.

Q1: What is the maximum amount I can borrow in a cash-out refinance?

In Canada, you can typically refinance up to 80% of your home’s appraised value. The remaining 20% must stay in the home as equity.

Q2: Will refinancing affect my current interest rate?

Yes, refinancing involves breaking your current mortgage contract and starting a new one. This means you will be subject to current market rates, which could be higher or lower than your existing rate.

Q3: What costs are involved in refinancing?

Common costs include a prepayment penalty for breaking your current term early, legal fees, and an appraisal fee. We calculate these upfront to ensure the refinance makes financial sense.

Q4: Can I refinance if I have bad credit?

It is more challenging, but possible. As a broker, I have access to alternative lenders who may assist homeowners with equity even if their credit score is less than perfect.

Q5: How long does the refinancing process take in Edmonton?

Typically, a refinance takes between 2 to 4 weeks from application to funding, depending on how quickly we can secure an appraisal and complete the legal paperwork.

{kind=link}

{kind=link}