Understanding the 2026 Mortgage Renewal Wave in Edmonton

If you secured a historically low mortgage rate back in 2021, you are likely part of the looming 2026 renewal wave. Edmonton homeowners who locked in five-year fixed rates around the 2 percent mark are now facing a very different financial landscape. With current rates hovering significantly higher, preparing early is the key to avoiding severe payment shock.

As an award-winning professional at Edmonton Mortgage Broker, Jason Scott has guided countless clients through volatile markets. The YEG real estate market is dynamic, and simply signing the first renewal letter your bank sends can cost you thousands of dollars. Taking a proactive approach allows you to explore independent advice, compare top lenders, and secure the best possible terms for your family’s budget.

Here are the primary factors driving the 2026 renewal concerns:

- Interest Rate Shifts: Transitioning from a pandemic-era low rate to current market rates can drastically increase monthly payments.

- Amortization Catch-Up: Variable rate holders with static payments may have seen their amortization periods extend, requiring larger payments upon renewal to get back on track.

- Lender Loyalty Penalties: Big banks often rely on client complacency, offering uncompetitive renewal rates to existing customers.

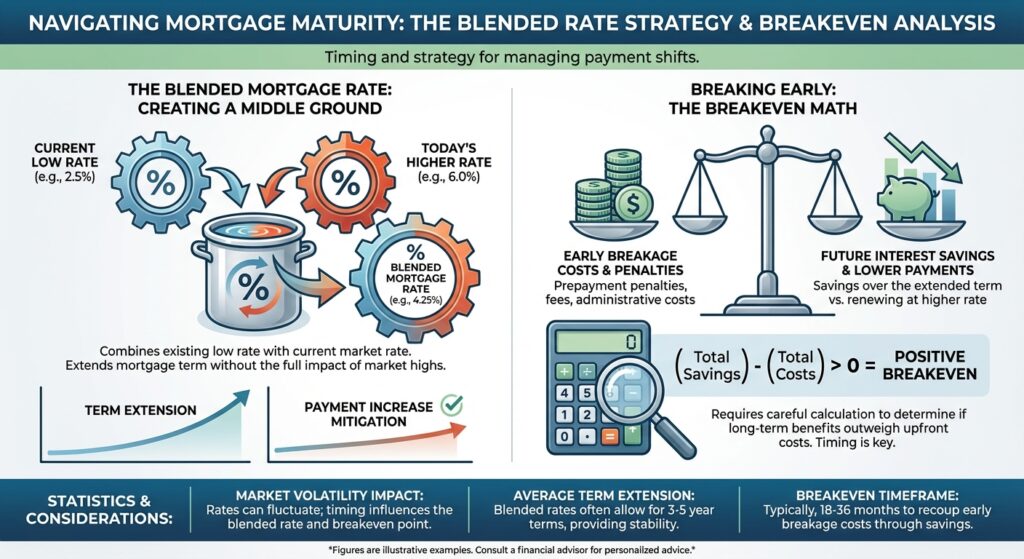

Timing Your Renewal and Exploring Blended Rates

Timing is everything when navigating your upcoming mortgage maturity. One of the most effective strategies to mitigate sudden payment increases is exploring a blended mortgage rate. This involves combining your current low rate with today’s higher rate to create a middle-ground interest rate, allowing you to extend your term without facing the full force of current market highs all at once.

However, breaking your current mortgage early requires careful breakeven math. You need to weigh the Interest Rate Differential (IRD) or three months’ interest penalty against the potential long-term savings of locking in a favorable rate today. By partnering with Jason Scott, Mortgage Broker, you gain access to independent access to top rates from over 20 lenders. We handle the heavy lifting, crunching the numbers to ensure that any early renewal or refinancing strategy genuinely puts money back in your pocket.

| Strategy | Current Rate (Until 2026) | Projected Renewal Rate | Estimated Monthly Payment (Based on $400k) | Payment Shock Impact |

|---|---|---|---|---|

| Wait Until 2026 Maturity | 2.10% | 4.50% (Estimated) | $2,215 | High (Sudden Increase) |

| Blend and Extend Today | Blended at 3.40% | N/A (New 5-Year Term) | $1,980 | Moderate (Gradual Adjustment) |

| Early Break & Renew | N/A (Penalty Paid) | 3.89% (Current Fixed) | $2,075 | Low (Requires Breakeven Math) |

Actionable Steps to Lower Your Monthly Costs Today

You do not have to wait until your renewal letter arrives in the mail to take control of your financial future. Edmonton homeowners can implement several smart strategies right now to soften the blow of the 2026 renewal wave.

First, take advantage of your pre-payment privileges. Most lenders allow you to increase your regular payments by 10 to 20 percent or make annual lump-sum payments directly toward your principal. Reducing your principal balance before renewal means you will be calculating your new, higher interest rate on a much smaller loan amount.

Consider these additional proactive steps:

- Secure a 120-Day Rate Hold: We can lock in a competitive rate up to four months before your renewal date, protecting you from unexpected rate hikes.

- Re-evaluate Your Amortization: If payment shock is too severe, refinancing to extend your amortization period back to 25 or 30 years can lower your monthly obligations, providing essential cash flow relief.

- Shop the Market: Never accept the first offer from your current bank. As an independent broker, Jason Scott shops the market for you, finding options that often beat big bank offers.

By leveraging an education-first approach, we ensure you understand every detail of your mortgage. Whether you are looking to consolidate debt or simply find the most competitive rate in Alberta, early preparation is your best defense against payment shock.

Q1: What is the 2026 mortgage renewal wave in Edmonton?

The 2026 renewal wave refers to the large number of homeowners who secured historically low mortgage rates around 2021 and will need to renew their terms at significantly higher current market rates, potentially leading to payment shock.

Q2: Should I break my mortgage early before my 2026 renewal?

It depends on the breakeven math. If the penalty to break your mortgage is lower than the long-term savings of locking in a favorable rate today, it makes sense. An independent mortgage broker can calculate this for you.

Q3: What is a blended mortgage rate?

A blended rate combines your current low interest rate with today’s higher market rate. This strategy allows you to access additional funds or extend your term without paying a massive penalty, resulting in a moderate rate between the two.

Q4: How early can I lock in a new mortgage rate in Alberta?

You can typically lock in a new mortgage rate up to 120 days before your maturity date. This rate hold protects you from potential interest rate increases while you finalize your renewal strategy.

Q5: Will my current bank offer me the best renewal rate?

Rarely. Banks often rely on the fact that most clients will not shop around. Working with an unbiased Edmonton mortgage broker gives you access to over 20 lenders, ensuring you get a highly competitive rate.

{kind=link}

{kind=link}