Understanding Mortgage Refinance Canada: Why Edmonton Homeowners Are Making the Move

If you are an Edmonton homeowner looking to optimize your financial strategy, a mortgage refinance might be the perfect solution. Navigating the landscape of mortgage refinance canada can feel overwhelming, but with the right guidance, it is a powerful tool to unlock your home’s equity, lower your monthly payments, or adjust your amortization period.

As your dedicated Edmonton mortgage broker, Jason Scott specializes in providing expert second opinions on mortgage refinancing. Often, homeowners accept the first renewal offer from their bank without realizing better options exist. Whether you want to explore a switch and transfer mortgage or simply want to know if breaking your current term is worth the penalty, we are here to provide unbiased, fact-checked advice tailored to the YEG market.

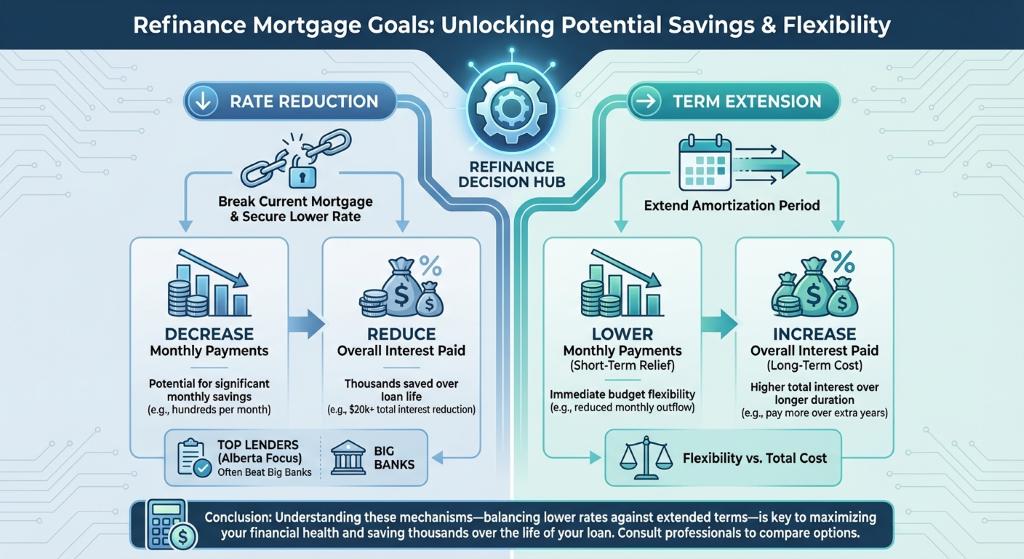

Key Benefits: Rate Reduction and Term Extension

When considering a refinance mortgage, two of the most common goals are rate reduction and term extension. Understanding how these mechanisms work can save you thousands of dollars over the life of your loan.

When considering a refinance mortgage, two of the most common goals are rate reduction and term extension. Understanding how these mechanisms work can save you thousands of dollars over the life of your loan.

- Rate Reduction: By breaking your current mortgage to secure a lower interest rate, you can significantly decrease your monthly payments and reduce the overall interest paid. We compare top lenders across Alberta to find rates that often beat the big banks.

- Term Extension: Extending your amortization period spreads your remaining balance over a longer timeframe. This lowers your immediate monthly financial obligations, freeing up cash flow for investments, renovations, or other life expenses.

Additionally, many Edmontonians leverage their home equity through a refinance with cash out to consolidate high-interest debt or fund major home improvements. Our goal is to ensure your mortgage aligns perfectly with your current financial reality.

| Mortgage Scenario | Interest Rate | Amortization Remaining | Estimated Monthly Payment |

|---|---|---|---|

| Current Mortgage | 5.50% | 20 Years | $2,750 |

| Refinance (Rate Reduction) | 4.25% | 20 Years | $2,450 |

| Refinance (Term Extension) | 4.50% | 25 Years | $2,100 |

Get a Second Opinion on Your Mortgage Refinance in Edmonton

In Edmonton’s dynamic real estate market, choosing the right mortgage broker means the difference between a confident financial decision and unnecessary stress. With over 15 years of experience in the YEG market, Jason Scott offers independent advice free from bank ties. We shop over 20 lenders to find competitive options tailored to your needs.

Getting a second opinion on your mortgage refinance is a smart, risk-free move. We will review your current terms, calculate potential penalties, and determine if a refinance mortgage truly benefits your bottom line. Do not leave money on the table; let us help you build a proactive mortgage management strategy to reach your mortgage freedom day sooner.

Q1: What is the main difference between a mortgage renewal and a mortgage refinance?

A renewal occurs at the end of your term when you sign a new contract for the remaining balance. A mortgage refinance involves replacing your existing mortgage with a completely new loan, which allows you to change the loan amount, rate, or amortization period before the current term ends.

Q2: Can I refinance my Edmonton home to consolidate debt?

Yes, refinancing to consolidate debt is very common. By accessing your home equity, you can pay off high-interest credit cards or loans, rolling them into your mortgage at a much lower interest rate to improve your monthly cash flow.

Q3: Will I pay penalties to break my current mortgage early?

Breaking a closed mortgage before the term ends usually incurs a prepayment penalty. However, as experts in mortgage refinance canada, we calculate these penalties for you to ensure the long-term savings of a lower rate or better terms outweigh the upfront costs.

Q4: How much equity do I need to qualify for a refinance mortgage?

In Canada, you can typically refinance up to 80% of your home’s appraised value. This means you must leave at least 20% equity in the property. We can help assess your Edmonton property’s current value to see what you qualify for.

Q5: Why should I get a second opinion on my refinance offer?

Banks often offer their existing clients less competitive rates, assuming they will not shop around. Getting a second opinion from an independent Edmonton mortgage broker ensures you are seeing the best rates from over 20 different lenders, potentially saving you thousands.

Contact Jason Scott Today for Your Free Refinance Consultation

{kind=link}

{kind=link}