Navigating the First-Time Buyer Mortgage Process in Canada

Stepping into the Edmonton real estate market is an exciting milestone. Securing your First-Time Homebuyer Mortgage (often referred to simply as a First-Time Buyer Mortgage) is the critical first step to making your dream of homeownership a reality. If you are exploring options for a first time home buyer mortgage canada, you need expert guidance to navigate the complexities of interest rates, lender policies, and government incentives.

As your dedicated Edmonton mortgage broker, Jason Scott and the team at TMG The Mortgage Group are here to simplify the process. We are experts at providing second opinions on first-time homebuyer mortgages, ensuring you never leave money on the table. Whether you are curious about leveraging the new First Home Savings Account (FHSA) or exploring down payment assistance programs, we tailor our advice to your unique financial situation.

- Unbiased Advice: We compare top lenders to find your best fit.

- Local Expertise: Deep knowledge of the Edmonton market and provincial guidelines.

- Stress-Free Pre-Approvals: Lock in your rate and shop with absolute confidence.

Essential Tax Credits, Rebates, and Savings Programs

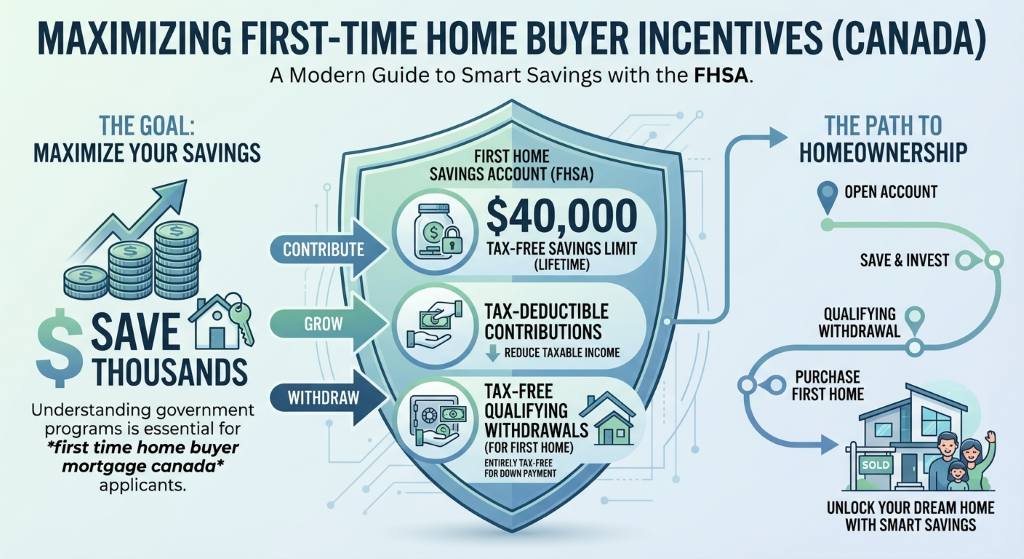

When applying for a First-Time Buyer Mortgage, maximizing your available government incentives can save you thousands of dollars. Understanding these programs is essential for any first time home buyer mortgage canada applicant.

When applying for a First-Time Buyer Mortgage, maximizing your available government incentives can save you thousands of dollars. Understanding these programs is essential for any first time home buyer mortgage canada applicant.

First Home Savings Account (FHSA)

The FHSA is a powerful tool for prospective homeowners. It allows you to save up to $40,000 tax-free for your down payment. Contributions are tax-deductible, and qualifying withdrawals to purchase your first home are entirely tax-free. Combining this with a Home Buyers Plan RRSP withdrawal can significantly boost your purchasing power.

Home Buyers Tax Credit

The Home Buyers Tax Credit provides a non-refundable tax credit to help recover closing costs such as legal expenses and inspections. This federal incentive offers up to $1,500 in tax relief for qualifying first-time buyers, making your transition into homeownership much smoother.

GST HST Rebate and Provincial Programs

If you are purchasing a newly built home or undergoing substantial renovations in Alberta, you might qualify for the GST HST Rebate. This rebate recovers a portion of the tax paid on the purchase price. Additionally, various provincial programs exist to assist Edmonton buyers with manageable down payment structures and reduced borrowing costs.

| Program Name | Maximum Benefit | Key Advantage |

|---|---|---|

| First Home Savings Account (FHSA) | Up to $40,000 lifetime contribution | Tax-deductible contributions and tax-free withdrawals |

| Home Buyers Plan (HBP) | Up to $60,000 RRSP withdrawal | Access retirement funds tax-free for a down payment |

| Home Buyers Tax Credit | $1,500 tax relief | Helps offset closing costs and legal fees |

| GST/HST New Housing Rebate | Varies by home purchase price | Recovers a portion of taxes on new builds |

Why Get a Second Opinion on Your Mortgage?

Many buyers accept the first mortgage offer they receive from their primary bank. However, choosing the wrong lender can cost you thousands in hidden fees and higher interest rates over your term. That is why we highly recommend getting a second opinion.

We are experts at providing second opinions on first-time homebuyer mortgages. By reviewing your current pre-approval or offer, Jason Scott can identify opportunities for better rates, more flexible prepayment privileges, and lower penalties. In Edmonton’s dynamic real estate market, having an independent broker on your side ensures you secure the most competitive first time home buyer mortgage canada has to offer.

Whether you are looking at neighborhoods like Oliver or Strathcona, having the right financial strategy in place will give you the confidence to make a winning offer.

Q1: What is the minimum down payment for a first-time homebuyer in Edmonton?

For homes under $500,000, the minimum down payment is 5%. For properties priced between $500,000 and $1.5 million, you will need 5% on the first $500,000 and 10% on the remaining balance.

Q2: Can I use both the FHSA and the Home Buyers Plan for my down payment?

Yes, you can combine funds from your First Home Savings Account and your RRSP Home Buyers Plan to maximize your down payment and reduce your overall mortgage size.

Q3: Why should I get a second opinion on my mortgage pre-approval?

Bank offers are limited to their specific products. A mortgage broker shops over 20 lenders to find lower rates and better terms, which can save you thousands of dollars over the life of your loan.

Q4: Are there specific provincial programs for first-time buyers in Alberta?

Alberta buyers can take advantage of federal programs like the Home Buyers Tax Credit and the FHSA, along with the GST HST Rebate for newly constructed homes.

Q5: Does a first-time buyer need mortgage default insurance?

If your down payment is less than 20%, you are required to obtain mortgage default insurance (often through CMHC). This protects the lender and allows you to secure competitive interest rates.

Ready to secure your First-Time Buyer Mortgage?

Get expert advice and save thousands on your home purchase.

{kind=link}

{kind=link}