Navigating Rental and Investment Property Mortgages in Edmonton

Investing in real estate is one of the most effective ways to build long-term wealth, but securing the right financing is crucial. Whether you are eyeing a duplex in Strathcona or expanding your portfolio with a multi-unit rental, understanding the nuances of an investment property mortgage canada is your first step to success.

As your dedicated Edmonton mortgage broker, Jason Scott and the team at TMG The Mortgage Group are here to help you navigate the complexities of a rental property mortgage. We specialize in providing expert second opinions on investment property mortgages, ensuring you are not leaving money on the table. Choosing the wrong lender can cost you thousands in interest and limit your cash flow. By comparing top lenders, we find the ideal financing strategy tailored to your real estate goals.

- Unbiased Advice: We work for you, not the banks, offering independent strategies for Edmonton investors.

- Customized Solutions: From single-family rentals to multi-unit properties, we structure your mortgage to maximize returns.

- Second Opinions: Already have a quote? Let us review it to ensure you are getting the best possible terms and rates.

Financing Multi-Unit Rentals and Commercial-Residential Hybrids

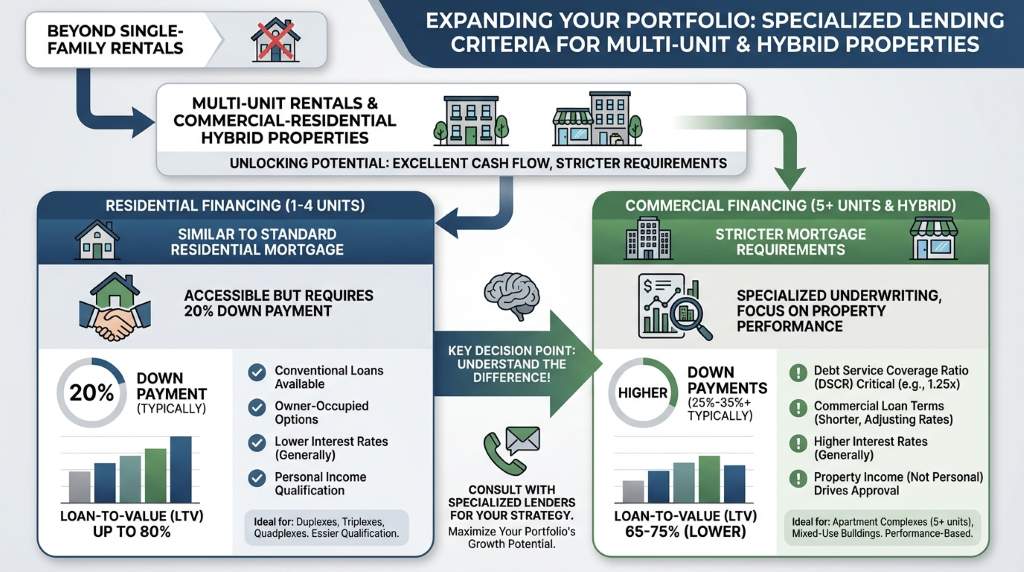

Expanding your portfolio beyond a standard single-family rental requires a deep understanding of specialized lending criteria. Multi-unit rentals and commercial-residential hybrid properties offer excellent cash flow potential, but they also come with stricter mortgage requirements.

Expanding your portfolio beyond a standard single-family rental requires a deep understanding of specialized lending criteria. Multi-unit rentals and commercial-residential hybrid properties offer excellent cash flow potential, but they also come with stricter mortgage requirements.

For properties with up to four units, you can often secure financing similar to a standard residential mortgage. However, investors must typically provide a 20 percent down payment. If you are considering a property with five or more units, or a commercial-residential hybrid, the financing shifts into the commercial lending sphere. Lenders will heavily scrutinize the property’s debt service coverage ratio, meaning the rental income must comfortably cover the mortgage payments and operating expenses.

When structuring these loans, many investors opt for a conventional fixed rate mortgage to lock in predictable monthly payments, which makes calculating long-term ROI much easier. If you are unsure which path aligns with your investment strategy, our team provides the holistic support and expert guidance needed to make confident, profitable decisions in the Edmonton real estate market.

| Property Type | Typical Down Payment | Mortgage Classification | Key Qualification Focus |

|---|---|---|---|

| Single-Family Rental | 20% | Residential Investment | Personal Income & Credit |

| Multi-Unit (2 to 4 Units) | 20% | Residential Investment | Personal Income & Projected Rent |

| Multi-Unit (5+ Units) | Varies (Often 25%+) | Commercial Mortgage | Property Debt Service Coverage Ratio |

| Commercial-Residential Hybrid | Varies (Often 25% to 30%) | Commercial Mortgage | Business Viability & Rental Yield |

Why You Need a Second Opinion on Your Investment Mortgage

In Edmonton’s dynamic real estate market, accepting the first mortgage offer you receive from your primary bank is rarely the best strategy. Lenders have vastly different policies regarding how they calculate rental income, which can significantly impact your borrowing power. This is why getting a second opinion on your investment property mortgage is critical.

At Jason Scott at TMG The Mortgage Group, we leverage our independent access to over 20 top lenders to find terms that protect your bottom line. We analyze the fine print, from interest rate differentials to pre-payment privileges, ensuring your mortgage works as hard as your investments do. Whether you are a seasoned investor or buying your first income property, we provide the education-first approach you need to thrive.

Do not let poor financing limit your portfolio’s growth. Reach out to us today to explore competitive rates, flexible terms, and customized solutions designed specifically for Canadian real estate investors.

Q1: What is the minimum down payment for an investment property mortgage in Canada?

For a standard rental property that you do not plan to live in, Canadian lenders require a minimum down payment of 20 percent. This applies to properties with one to four units.

Q2: Can I use potential rental income to qualify for my mortgage?

Yes, most lenders allow you to use a portion of the projected or actual rental income to help qualify for the mortgage. However, each lender has different rules on how much of that income can be used, which is why working with an expert broker is beneficial.

Q3: What is the difference between a residential and commercial investment mortgage?

Residential investment mortgages typically apply to properties with one to four units. Once a property has five or more units, or if it is a commercial-residential hybrid, it requires a commercial mortgage, which involves stricter qualification metrics based on the property’s revenue.

Q4: Why should I get a second opinion on my rental property mortgage?

Lenders treat rental portfolios differently. A second opinion ensures you are getting the most favorable terms, the best interest rates, and a mortgage structure that maximizes your borrowing power and cash flow.

Q5: Are mortgage interest rates higher for investment properties?

Yes, interest rates for investment properties are generally slightly higher than those for primary residences because lenders view them as a higher risk. However, an independent broker can shop around to find you the most competitive rate available.

Ready to maximize your real estate ROI? Contact Jason Scott today at 1-780-721-4879 or email jason@edmontonmortgagebroker.com to secure the best investment property mortgage for your Edmonton portfolio!

{kind=link}

{kind=link}