What is a Cashback Mortgage and How Does It Work in Edmonton?

If you are buying a home in Edmonton, AB, you might be looking for ways to cover upfront costs like legal fees, moving expenses, or immediate renovations. This is where a Cash-Back Mortgage (also known as a Cashback Mortgage) comes into play. A cash back mortgage Canada program provides you with a lump sum of cash right when your mortgage closes. Typically ranging from 1% to 5% of your total mortgage amount, this cash can be a lifesaver for new homeowners who need extra liquidity.

However, these mortgages come with specific terms and conditions. They are most commonly offered as a closed-mortgage, which means you commit to a specific term length and interest rate. As an experienced Edmonton mortgage broker, Jason Scott and the team at TMG The Mortgage Group are experts at providing second opinions on cash-back mortgages. We help you understand if the upfront cash is actually worth the potentially higher interest rate compared to standard lending options.

Comparing Closed and Open Mortgages for Your Cash Back Strategy

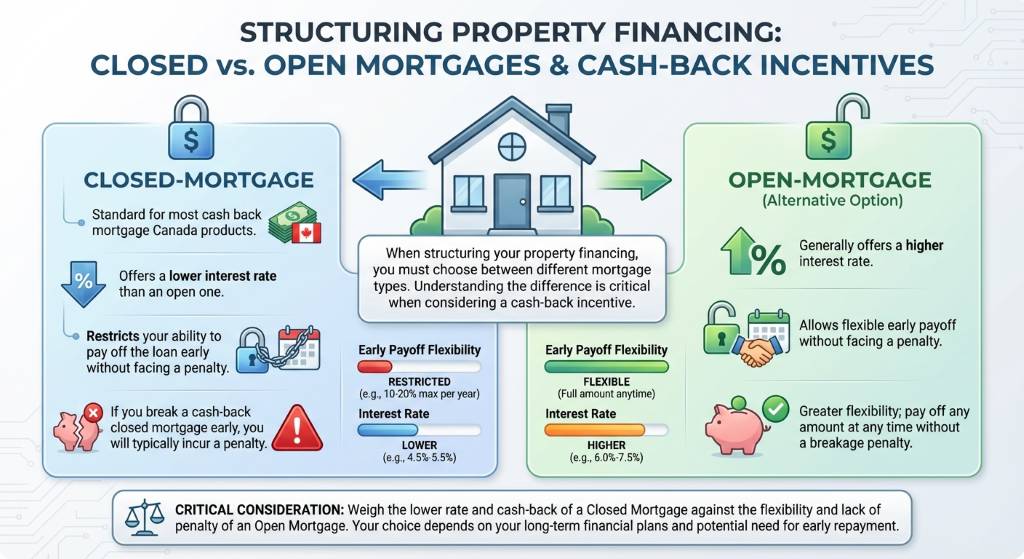

When structuring your property financing, you must choose between different mortgage types. Understanding the difference between a closed and an open-mortgage is critical when considering a cash-back incentive.

When structuring your property financing, you must choose between different mortgage types. Understanding the difference between a closed and an open-mortgage is critical when considering a cash-back incentive.

- Closed-Mortgage: This is the standard for most cash back mortgage Canada products. A closed mortgage offers a lower interest rate than an open one but restricts your ability to pay off the loan early without facing a penalty. If you break a cash-back closed mortgage early, you will typically have to repay a prorated portion of the cash back you received.

- Open-Mortgage: An open mortgage gives you the ultimate flexibility to pay off your entire mortgage balance at any time without penalties. However, lenders rarely offer cash-back incentives on open mortgages because they need the security of a fixed term to recoup the cost of the cash advance.

We highly recommend getting a professional second opinion before signing any paperwork. Choosing the wrong lender or mortgage type can cost you thousands in the long run. Let us analyze your Edmonton real estate goals to see which path makes the most financial sense for you.

| Feature | Cash-Back Mortgage | Standard Mortgage |

|---|---|---|

| Upfront Cash Provided | Yes (Usually 1% to 5% of loan amount) | No upfront cash provided |

| Interest Rates | Typically higher (Posted rates apply) | Discounted rates widely available |

| Mortgage Type | Usually a 5-year closed-mortgage | Available as closed or open-mortgage |

| Early Break Penalties | Standard penalty plus prorated cash-back repayment | Standard IRD or 3-months interest penalty |

Why You Need a Second Opinion on Your Cash-Back Mortgage

In Edmonton’s dynamic real estate market, a cash-back mortgage can seem incredibly appealing. Who would not want extra funds to furnish a new home in Strathcona or cover closing costs in Oliver? However, banks often charge their higher posted interest rates for these products rather than their best-discounted rates. Over a five-year term, the extra interest you pay might far exceed the initial cash bonus you received.

This is exactly why we are experts at providing second opinions on cash-back mortgages. Jason Scott has over 15 years of experience in the YEG real estate market, offering independent advice completely free from bank ties. We will run the numbers, compare the long-term costs, and show you exactly what you are paying for that upfront cash. Whether you are a first-time buyer or looking to refinance, our personalized strategies are designed to help you save thousands and reach mortgage freedom faster.

Q1: What is a cash back mortgage Canada?

A cash back mortgage provides a lump sum of cash to the borrower upon closing. This is typically a percentage of the total mortgage amount and can be used for things like closing costs, renovations, or debt consolidation in Edmonton, AB.

Q2: Can I get a cash-back incentive on an open-mortgage?

Generally, no. Lenders almost exclusively offer cash-back incentives on closed-mortgages, usually with a 5-year term, to ensure they can recover the cost of the cash advance through guaranteed interest payments.

Q3: What happens if I break my cash-back mortgage early?

If you have a closed-mortgage with a cash-back feature and you break it before the term ends, you will have to pay standard mortgage break penalties plus a prorated repayment of the cash back you initially received.

Q4: Are interest rates higher on a Cashback Mortgage?

Yes, lenders typically apply their posted interest rates rather than discounted rates for cash-back mortgages. This is why getting a second opinion from an Edmonton mortgage broker like Jason Scott is vital to ensure it is the right financial move.

Q5: How can a second opinion save me money on my mortgage?

A second opinion allows an independent broker to compare the true cost of a cash-back mortgage against standard options. We calculate the total interest paid over the term versus the cash received, ensuring you do not overpay for your Edmonton home financing.

{kind=link}

{kind=link}