Understanding the Basics of an Open-Term Mortgage

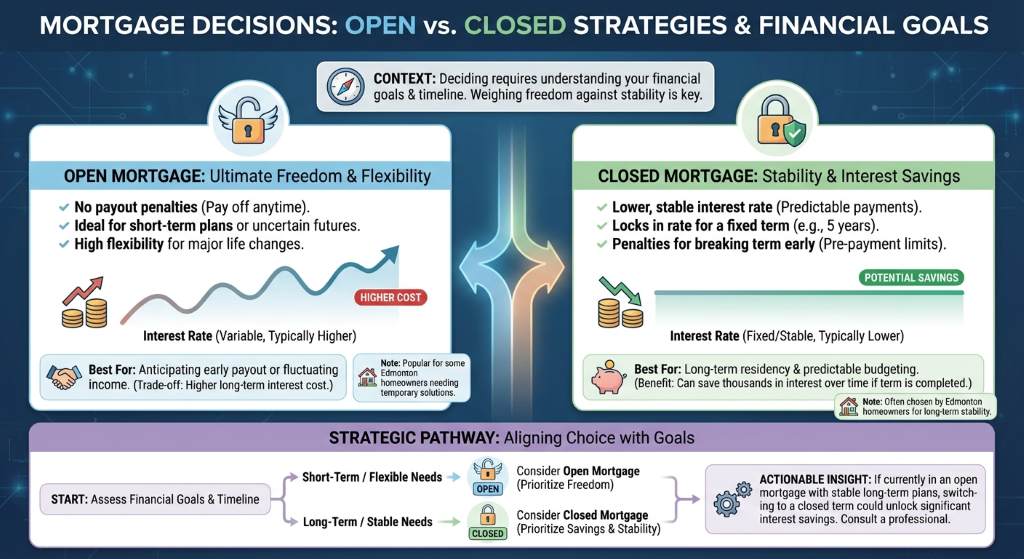

When navigating the Edmonton real estate market, choosing the right financing is crucial. An open mortgage, also widely known as an open-term mortgage, offers unparalleled flexibility for homeowners. If you are exploring an open mortgage Canada residents often find this option appealing because it allows you to pay off your mortgage in part or in full at any time without facing prepayment penalties.

Unlike a closed-mortgage which restricts how much extra you can pay each year, an open mortgage gives you the freedom to make large lump-sum payments or even clear the entire balance whenever you choose. This is particularly beneficial if you are expecting a significant influx of cash, such as an inheritance, a large bonus, or proceeds from selling another property.

- Total Flexibility: Pay down your principal balance faster without penalty fees.

- Short-Term Solutions: Ideal if you plan to sell your Edmonton home in the near future.

- Peace of Mind: Avoid the stress of being locked into a rigid contract.

However, this flexibility comes at a cost. Open mortgages typically carry higher interest rates compared to closed alternatives. As an experienced Edmonton mortgage broker, I specialize in providing expert second opinions on open mortgages to ensure you are not paying more interest than necessary.

Comparing Open Mortgages to Closed and Switch Options

Deciding between different mortgage products requires a clear understanding of your financial goals. While an open mortgage offers ultimate freedom, it is important to weigh it against other strategies.

Deciding between different mortgage products requires a clear understanding of your financial goals. While an open mortgage offers ultimate freedom, it is important to weigh it against other strategies.

For many Edmonton homeowners, a closed mortgage provides a lower, more stable interest rate. If you do not anticipate paying off your mortgage early, locking into a closed term can save you thousands of dollars in interest over time. On the other hand, if you currently have an open mortgage and want to secure a lower rate, you might consider a switch-and-transfer-mortgage. Switching your mortgage to a new lender or transferring to a closed term can significantly reduce your monthly payments.

Here is when you should consider switching or transferring:

- Your financial situation has stabilized, and you no longer need the flexibility to make massive lump-sum payments.

- You want to take advantage of lower interest rates currently available in the Edmonton market.

- You are looking to consolidate debt or unlock home equity.

Getting a second opinion is always a smart move. At Jason Scott TMG The Mortgage Group, we analyze your current open-term mortgage and compare it against top lenders to see if a switch and transfer strategy is your most profitable path forward.

| Feature | Open Mortgage | Closed Mortgage |

|---|---|---|

| Prepayment Penalties | None | Yes (often 3 months interest or IRD) |

| Interest Rates | Typically Higher | Typically Lower |

| Flexibility | Maximum freedom to pay off early | Limited to specific annual privileges (e.g., 15%) |

| Best Suited For | Short-term owners, those expecting large cash windfalls | Long-term homeowners seeking rate stability |

Expert Second Opinions on Your Open Mortgage in Edmonton

Choosing the wrong lender or staying in an open mortgage longer than necessary can cost you thousands in extra interest. In Edmonton’s dynamic real estate market, having an independent mortgage broker on your side means you get unbiased advice tailored to your unique financial situation.

We are experts at providing second opinions on open mortgages. Whether you are living in Strathcona, Oliver, or anywhere else in the Edmonton area, we will review your current terms, assess your future goals, and help you determine if an open mortgage remains your best choice or if transitioning to a closed mortgage makes more financial sense.

With independent access to over 20 top lenders, we often find rates that beat the big banks. Let us handle the heavy lifting so you can enjoy a stress-free process and become mortgage-free faster. Reach out to Jason Scott at 780-721-4879 or email jason@edmontonmortgagebroker.com to discuss your options.

Q1: What is an open mortgage in Canada?

An open mortgage in Canada allows you to pay off your mortgage partially or in full at any time without incurring prepayment penalties. It is highly flexible but usually comes with a higher interest rate compared to closed mortgages.

Q2: Can I switch from an open mortgage to a closed mortgage?

Yes, you can easily transition from an open-term mortgage to a closed mortgage. This is often done through a switch-and-transfer-mortgage process, allowing you to lock in a lower interest rate once you no longer need the flexibility of open terms.

Q3: Why are interest rates higher on an open mortgage?

Lenders charge higher interest rates on open mortgages to compensate for the flexibility they provide. Because you can pay off the loan at any time, the lender takes on more risk regarding their expected interest earnings.

Q4: Is an open mortgage a good idea for a first-time home buyer in Edmonton?

Generally, first-time buyers in Edmonton opt for closed mortgages to secure lower payments and stability. However, if a buyer expects a massive cash windfall shortly after purchasing, an open mortgage might temporarily make sense. We highly recommend getting a second opinion to be sure.

Q5: Do I have to pay a penalty to break an open mortgage?

No, the defining feature of an open mortgage is that there are no prepayment penalties. You can break it, pay it off, or refinance it at any time without paying the costly fees associated with breaking a closed mortgage.

{kind=link}

{kind=link}