Understanding Bad Credit Mortgages in Canada

Life happens, and sometimes your credit score takes a hit. If you have been turned down by traditional banks, you might think buying a home or refinancing is out of reach. However, a bad credit mortgage (also known as a poor credit mortgage or subprime mortgage) can provide the financial bridge you need. Navigating a bad credit mortgage canada wide, and specifically right here in Edmonton, AB, requires expert guidance to ensure you get the best possible terms.

As an award-winning Edmonton mortgage broker, Jason Scott and his team specialize in helping clients who have faced financial setbacks. We are experts at providing second opinions on bad credit mortgage applications. If a bank has said no, let us take a look. We have access to alternative lending solutions that focus on your overall financial health and home equity rather than just a three-digit credit score.

B-Lender and Private Mortgage Options for Poor Credit

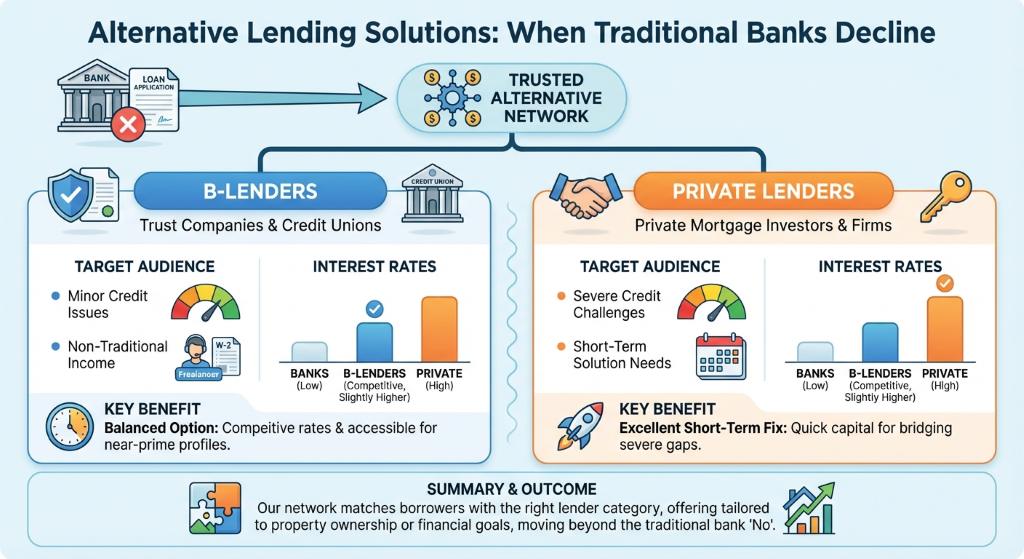

When traditional banks decline an application, we turn to our trusted network of alternative lenders. These generally fall into two categories:

When traditional banks decline an application, we turn to our trusted network of alternative lenders. These generally fall into two categories:

- B-Lenders: These are trust companies and credit unions that offer mortgages to individuals with minor credit issues or non-traditional income. They offer competitive rates that are slightly higher than banks but much lower than private options.

- Private Lenders: A private mortgage is an excellent short-term solution for those with severe credit challenges. Private lenders care more about the equity in your home and its marketability than your credit score.

Many Edmonton homeowners use these alternative options to access second mortgages. This allows you to tap into your home equity without breaking your favorable first mortgage. Furthermore, if high-interest debt is the root cause of your low credit score, securing debt consolidation loans through a subprime mortgage can help you pay off creditors, improve your monthly cash flow, and rebuild your credit over time.

| Lender Type | Minimum Credit Score | Income Verification | Primary Focus |

|---|---|---|---|

| A-Lender (Banks) | 600 to 680+ | Strict (T4, NOA) | Credit History & Low Debt Ratios |

| B-Lender (Trusts) | 500 to 599 | Flexible (Stated Income allowed) | Steady Income & Down Payment |

| Private Lenders | No Minimum | Very Flexible | Property Value & Home Equity |

Why Get a Second Opinion on Your Mortgage Application?

Being denied a mortgage by your primary bank is discouraging, but it should never be the end of your homeownership journey. We highly recommend getting a second opinion. Because we operate independently of the big banks, we can shop your application across over twenty different lenders. We know exactly which institutions are currently offering the most favorable terms for a bad credit mortgage in Edmonton.

Our goal is not just to get you approved today, but to set you up for long-term financial success. We will create a customized strategy that helps you transition from a subprime mortgage back to a prime lender once your credit improves. Whether you are looking to buy a new home in Strathcona or refinance your property in Oliver, our expert team will guide you step by step to ensure you make confident and informed mortgage decisions.

Q1: What is a bad credit mortgage?

A bad credit mortgage, or subprime mortgage, is a home loan designed for borrowers with low credit scores who do not qualify for traditional bank financing. It provides a path to homeownership or refinancing while you work on rebuilding your credit.

Q2: Can I get a mortgage with bad credit in Edmonton?

Yes, you can. We work with specialized B-Lenders and private investors in Alberta who focus on your home equity and overall financial picture rather than just your credit score.

Q3: Are interest rates higher for poor credit mortgages?

Yes, because alternative lenders take on more risk, the interest rates are typically higher than those offered by major banks. However, these are often designed as short-term solutions to help you transition back to prime rates once your credit improves.

Q4: How can a second mortgage help my credit?

Taking out a second mortgage can provide the funds needed to consolidate high-interest debts. Paying off multiple credit cards and personal loans can significantly boost your credit score over time while improving your monthly cash flow.

Q5: Do you offer second opinions if my bank declined me?

Absolutely. We are experts at providing second opinions on bad credit mortgage applications. We review your unique situation to find alternative lending options and strategies that your primary bank cannot offer.

Ready to explore your mortgage options?

Contact Jason Scott today at 1-780-721-4879 or email jason@edmontonmortgagebroker.com.

{kind=link}

{kind=link}