Understanding the No-Frills Low-Rate Minimal-Service Mortgage

When shopping for a home in Edmonton, AB, you might come across the term no-frills low-rate minimal-service mortgage. Also known simply as a no-frills mortgage, this financial product is designed for borrowers who want the absolute lowest interest rate possible and are willing to sacrifice standard mortgage features to get it.

A primary keyword base for many home buyers is finding a competitive no frills mortgage canada, but it is vital to understand exactly what you are signing up for. Typically structured as a strict closed-mortgage, a no-frills option restricts your flexibility. You will generally face severe limitations on pre-payment privileges, meaning you cannot easily pay down your principal faster without incurring significant penalties.

- Lower Interest Rates: The main draw is a highly discounted rate compared to standard products.

- Minimal Services: Lenders offer fewer customer service perks and strict contract terms.

- Bona Fide Sales Clause: Many no-frills mortgages cannot be broken before the term ends unless you actually sell the property.

As experts at providing second opinions on no-frills low-rate mortgages, Jason Scott and the team at Edmonton Mortgage Broker can help you determine if the upfront savings are worth the long-term restrictions.

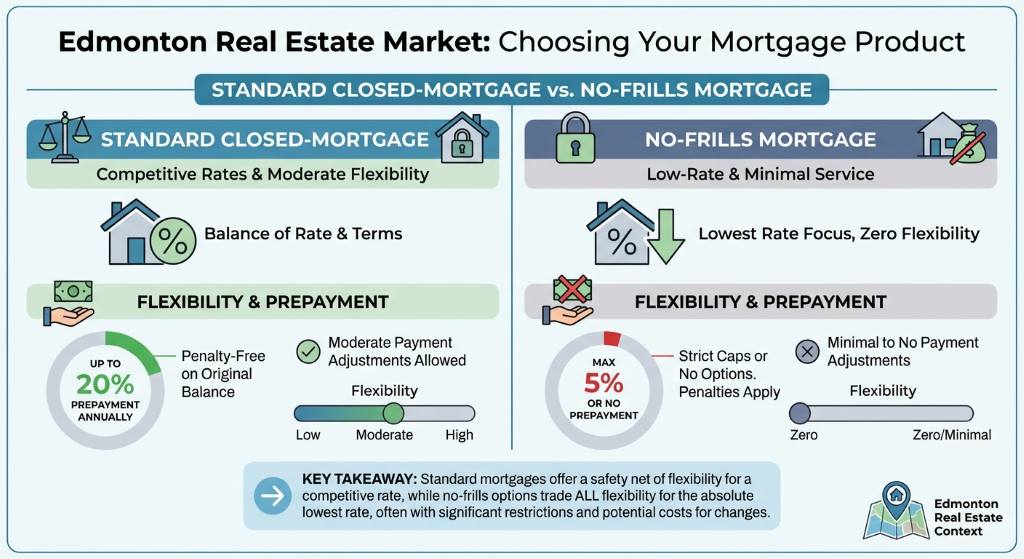

How a No-Frills Mortgage Compares to a Standard Closed-Mortgage

In the dynamic Edmonton real estate market, choosing the right mortgage product is crucial. While a standard closed-mortgage offers a balance of competitive rates and moderate flexibility, a no-frills mortgage strips away that flexibility entirely.

In the dynamic Edmonton real estate market, choosing the right mortgage product is crucial. While a standard closed-mortgage offers a balance of competitive rates and moderate flexibility, a no-frills mortgage strips away that flexibility entirely.

For example, a standard mortgage might allow you to prepay up to 20 percent of your original balance each year penalty-free. A no-frills low-rate minimal-service mortgage might cap this at 5 percent, or offer no prepayment options at all. Furthermore, if you need to break your mortgage to refinance or access equity, the penalties on a no-frills product are often calculated using a much higher interest rate differential (IRD).

Before signing on the dotted line for the lowest rate you see online, review the data below to see how a standard closed product stacks up against a minimal-service option. Getting a second opinion from an independent Edmonton mortgage broker can save you thousands in hidden fees down the road.

| Feature | Standard Closed-Mortgage | No-Frills Mortgage |

|---|---|---|

| Interest Rate | Competitive | Ultra-Low (Discounted) |

| Prepayment Privileges | 10% to 20% annually | 0% to 5% annually |

| Portability | Usually portable to a new home | Often restricted or not allowed |

| Early Break Penalty | Standard IRD or 3 months interest | High IRD or strict bona fide sales clause |

| Best Suited For | Borrowers needing some flexibility | Borrowers certain they will not move or refinance |

Expert Second Opinions on Your Edmonton Mortgage Options

It is easy to be tempted by the rock-bottom rates of a no frills mortgage canada offers, but those initial savings can quickly vanish if life circumstances change. Whether you are a first-time homebuyer in Strathcona or looking to renew your mortgage in Oliver, having an unbiased expert review your contract is essential.

At Edmonton Mortgage Broker, Jason Scott leverages over 15 years of local YEG real estate experience to provide independent advice free from bank ties. We are experts at providing second opinions on no-frills low-rate mortgages. We will carefully analyze the fine print of any closed-mortgage offer to ensure you are not trapped by restrictive clauses or exorbitant break penalties.

Our goal is to empower you with personalized strategies to save thousands, offering stress-free local support every step of the way. Do not let a minimal-service mortgage cost you your financial freedom.

Q1: What is a no-frills mortgage in Canada?

A no-frills mortgage is a highly discounted loan that offers a lower interest rate in exchange for minimal flexibility, strict penalties, and limited prepayment options.

Q2: Is a no-frills mortgage the same as a closed-mortgage?

Yes, it is a specific type of closed-mortgage. However, while standard closed mortgages offer some flexibility, a no-frills option strips away almost all standard features like portability and prepayment privileges.

Q3: Can I break a no-frills low-rate minimal-service mortgage early?

Often, you cannot break it at all unless you sell the property (known as a bona fide sales clause). If you are allowed to break it, the financial penalties are typically much higher than standard mortgages.

Q4: Why should I get a second opinion on a no-frills mortgage offer?

Because the hidden restrictions can cost you thousands if you need to refinance, move, or pay off your loan early. An experienced Edmonton mortgage broker can spot these restrictive clauses before you sign.

Q5: Are no-frills mortgages a good idea for Edmonton homebuyers?

They can be, but only if you are absolutely certain you will not move, refinance, or want to make lump-sum payments during your term. Always consult with an expert to ensure it aligns with your long-term goals.

{kind=link}

{kind=link}