Understanding Conventional Fixed-Rate Mortgages in Edmonton

When navigating the Edmonton real estate market, choosing the right financing is crucial. A conventional fixed-rate mortgage offers unparalleled peace of mind by locking in your interest rate and monthly payment for the duration of your term. Whether you are a first-time buyer in Strathcona or upgrading your home in Oliver, understanding your options for a fixed rate mortgage canada can save you thousands over the life of your loan.

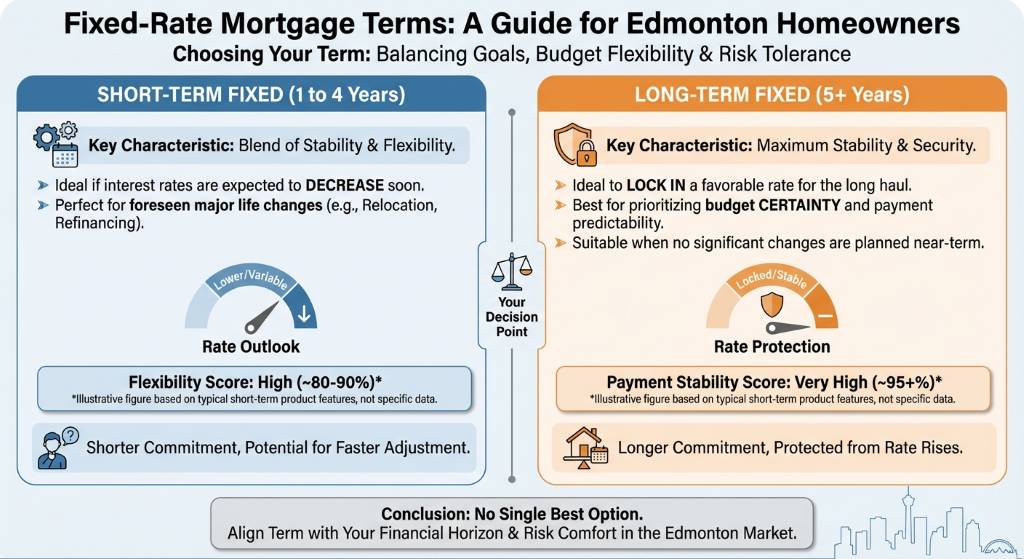

Fixed-rate terms generally fall into two broad categories:

- Short-term mortgages (1 to 4 years): Ideal if you anticipate a drop in interest rates, plan to move soon, or want the flexibility to reassess your finances in the near future.

- Long-term mortgages (5 to 10 years): Perfect for homeowners seeking long-term budget stability and protection against unpredictable rate hikes.

If you are unsure whether locking in your rate is the right move for your current financial situation, it is always a smart strategy to compare these options against a variable rate mortgage. As your dedicated Edmonton mortgage broker, Jason Scott provides the expert, unbiased advice you need to make confident decisions.

Short-Term vs. Long-Term Fixed-Rate Terms: Which is Right for You?

Choosing between a short-term and a long-term fixed-rate mortgage depends entirely on your financial goals, budget flexibility, and risk tolerance. Here is a closer look at what each option offers to Edmonton homeowners:

Choosing between a short-term and a long-term fixed-rate mortgage depends entirely on your financial goals, budget flexibility, and risk tolerance. Here is a closer look at what each option offers to Edmonton homeowners:

Short-Term Terms (1 to 4 Years)

Short-term fixed mortgages offer a blend of stability and flexibility. They are an excellent choice if you expect interest rates to decrease in the near future or if you foresee a major life change, such as relocating for work or refinancing to consolidate debt. While the rates might differ from longer terms, they prevent you from being locked into a lengthy contract, allowing you to renew or change lenders sooner.

Long-Term Terms (5 to 10 Years)

The 5 year fixed-rate mortgage is the most popular choice in Canada, striking a great balance between competitive rates and payment stability. Terms extending up to 7 or 10 years are available for those who want absolute certainty in their budgeting over an entire decade. This is especially valuable in a fluctuating economy where rate increases could otherwise impact your monthly cash flow.

We are experts at providing second opinions on conventional fixed-rate mortgages. If you have received a renewal offer from your current bank, let us review it to ensure you are getting the absolute best deal possible. Alternatively, if you want the best of both worlds, you might consider exploring a hybrid mortgage that blends fixed and variable elements to diversify your interest rate risk.

| Mortgage Term | Typical Rate Stability | Flexibility to Break/Renew | Best Suited For |

|---|---|---|---|

| 1 to 4 Years (Short-Term) | Moderate | High | Buyers expecting rate drops or those planning to move or refinance soon. |

| 5 Years (Standard) | High | Moderate | Most Canadian homeowners seeking a balanced mix of rate value and stability. |

| 7 to 10 Years (Long-Term) | Maximum | Low | Homeowners wanting long-term budget certainty and protection from rate hikes. |

Why Get a Second Opinion on Your Fixed-Rate Mortgage?

Many Edmontonians simply accept the first renewal letter or mortgage pre-approval offer their bank provides. However, choosing the wrong lender can cost you thousands in unnecessary interest and hidden fees. Because we operate independently from the big banks, we have access to over 20 top lenders across Canada, allowing us to shop the market on your behalf.

Getting a second opinion is quick, stress-free, and could uncover a much better rate or more favorable prepayment privileges. Whether you are a first-time buyer looking for a 5 percent down payment option or an experienced investor managing multiple properties, we tailor our strategies to help you become mortgage-free faster.

- Unbiased Expertise: We work exclusively for you, ensuring your financial interests always come before the bank’s profits.

- Personalized Strategies: We find custom prepayment options that allow you to pay down your principal faster without penalties.

- Local YEG Support: We offer a deep understanding of the Edmonton real estate market, connecting you with trusted local realtors and inspectors.

Do not leave your financial future to chance. Let our award-winning team review your fixed-rate mortgage offer today.

Q1: What is a conventional fixed-rate mortgage?

A conventional fixed-rate mortgage is a home loan where the interest rate and your monthly payments remain exactly the same for the duration of your chosen term, typically ranging from 1 to 10 years. This provides complete predictability for your budget.

Q2: Why should I choose a 5-year fixed rate mortgage in Canada?

The 5-year term is the most popular fixed rate mortgage in Canada because it offers an ideal middle ground between securing a highly competitive interest rate and maintaining long-term payment stability without a decade-long commitment.

Q3: Can I break my fixed-rate mortgage early?

Yes, but breaking a fixed-rate mortgage before the term ends usually results in a prepayment penalty. This penalty is typically calculated as the greater of three months of interest or the Interest Rate Differential (IRD).

Q4: How do short-term fixed mortgages differ from long-term ones?

Short-term mortgages (1 to 4 years) offer more flexibility and allow you to renew sooner, which is advantageous if rates drop. Long-term mortgages (5 to 10 years) provide maximum budget certainty but offer less flexibility to break the contract without incurring penalties.

Q5: Do you offer second opinions on bank mortgage offers?

Absolutely. We are experts at providing second opinions on conventional fixed-rate mortgages. We will compare your bank’s offer against products from over 20 lenders to ensure you are getting the best possible rate and terms available in Edmonton.

{kind=link}

{kind=link}