What is a HELOC and How Can Edmonton Homeowners Benefit?

If you own a home in Edmonton, you might be sitting on a significant amount of untapped wealth. A Home Equity Line of Credit (HELOC) is one of the most flexible financial tools available to homeowners today. Whether you are looking to fund a major home renovation, consolidate high-interest debt, or invest in additional property, understanding how a heloc canada works is the first step toward financial empowerment.

Unlike a traditional loan that provides a lump sum, a HELOC is a revolving line of credit secured by your home equity. This means you can borrow what you need, pay it back, and borrow again, much like a credit card but with significantly lower interest rates. As an expert Edmonton mortgage broker, Jason Scott specializes in helping clients navigate these options. We are experts at providing second opinions on HELOCs to ensure you are getting the absolute best terms possible.

Before diving into the specifics, it is important to know that you have multiple ways to access your home equity. Depending on your financial goals, you might also want to explore a home equity loan or second mortgage, or consider if you should refinance with cash out.

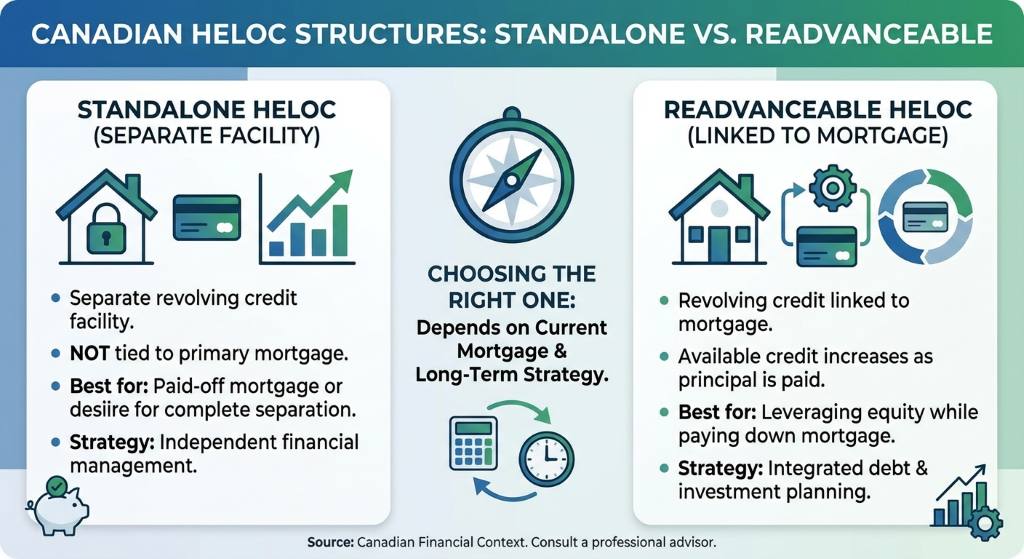

Standalone vs. Readvanceable: Which HELOC is Right for You?

When exploring a HELOC in Canada, you will generally encounter two main structures: standalone and readvanceable. Choosing the right one depends heavily on your current mortgage setup and long-term financial strategy.

When exploring a HELOC in Canada, you will generally encounter two main structures: standalone and readvanceable. Choosing the right one depends heavily on your current mortgage setup and long-term financial strategy.

- Standalone HELOC: This is a separate revolving credit facility that is not tied to your primary mortgage. It is an excellent choice if your primary mortgage is already paid off or if you want to keep your mortgage and your line of credit completely separate.

- Readvanceable HELOC: Often combined with your standard mortgage, a readvanceable mortgage automatically increases your available credit limit as you pay down your mortgage principal. This seamless integration is highly popular among Edmonton homeowners looking for ongoing access to funds without needing to reapply.

Not sure which option fits your lifestyle? Getting a second opinion on HELOCs can save you thousands in hidden fees and suboptimal interest rates. We review your current financial snapshot and compare top lenders to find your perfect fit.

| Feature | Standalone HELOC | Readvanceable HELOC |

|---|---|---|

| Structure | Separate from your primary mortgage | Combined with your primary mortgage |

| Credit Limit | Fixed maximum based on initial approval | Grows automatically as mortgage principal is paid |

| Best For | Homes with no mortgage or separate borrowing needs | Long-term flexibility and seamless borrowing |

| Application Process | Requires a separate application and appraisal | Set up once during the initial mortgage process |

Expert Advice for Securing the Best HELOC in Edmonton

Securing a HELOC in Canada requires a solid understanding of your property value, credit score, and lending rules. In Edmonton’s dynamic real estate market, choosing the wrong lender can cost you thousands in unnecessary interest. That is why partnering with an award-winning mortgage broker is crucial for your financial health.

As an independent broker, Jason Scott shops over 20 different lenders to find competitive options that often beat big bank offers. If you already have a quote from your bank, bring it to us! We are experts at providing second opinions on HELOCs and can often find a more flexible or cost-effective solution tailored to your specific needs.

Ready to unlock the wealth tied up in your home? It is time to make your equity work for you. Whether you need funds to upgrade your Edmonton property, invest, or consolidate debt, we provide stress-free, unbiased guidance every step of the way. Call us at 780-721-4879 to get started.

Q1: What is the maximum amount I can borrow with a HELOC in Canada?

In Canada, you can borrow up to 65% of your home’s appraised value through a standalone HELOC. However, your combined mortgage and HELOC cannot exceed 80% of the total value of your home.

Q2: Do I have to make monthly payments on my HELOC?

Yes, but one of the major benefits of a HELOC is that you are typically only required to make interest-only payments on the amount you have actually borrowed, making it very manageable for your monthly cash flow.

Q3: Can I use a HELOC to buy a second home or investment property in Edmonton?

Absolutely. Many Edmonton homeowners use their primary residence’s equity via a HELOC to fund the down payment for an investment property or a vacation home.

Q4: How does a readvanceable mortgage differ from a traditional mortgage?

A readvanceable mortgage links your traditional mortgage to a line of credit. As you pay down the principal balance of your mortgage, your available credit limit on the HELOC increases automatically by the same amount.

Q5: Why should I get a second opinion on my bank’s HELOC offer?

Banks often only offer their own restricted products. As an independent Edmonton mortgage broker, we compare multiple lenders to ensure you get the lowest rates, best terms, and a product that truly aligns with your financial goals.

in Canada){kind=link}

in Canada&description=&image=https://edmontonmortgagebroker.com/wp-content/uploads/2026/05/d5a56641-6bda-4256-9198-b9565976d317-1024x572.jpg){kind=link}