Understanding First Nations Mortgage Options and On-Reserve Loans

Navigating the path to homeownership can feel overwhelming, but specialized Indigenous First Nations Home Loan Programs are designed to make the process accessible and straightforward. Whether you are looking for a First Nations mortgage in Canada or exploring an on-reserve loan, understanding your options is the critical first step to securing your dream home.

As an experienced Edmonton mortgage broker, Jason Scott and the team at TMG The Mortgage Group are experts at providing second opinions on Indigenous and First Nations home loans. We know that securing financing on settlement lands or reserves comes with unique legal and structural requirements. From exploring standard residential mortgages to specialized Indigenous Home Loans, we offer unbiased advice tailored to your specific financial goals.

Many homebuyers also explore options like a high-ratio insured mortgage through CMHC or Sagen to help secure competitive rates with lower down payments. Our goal is to compare top lenders and find the perfect fit for your unique situation, saving you time, stress, and money.

Comprehensive Coverage: CMHC Section 95 and On-Reserve Non-Profit Programs

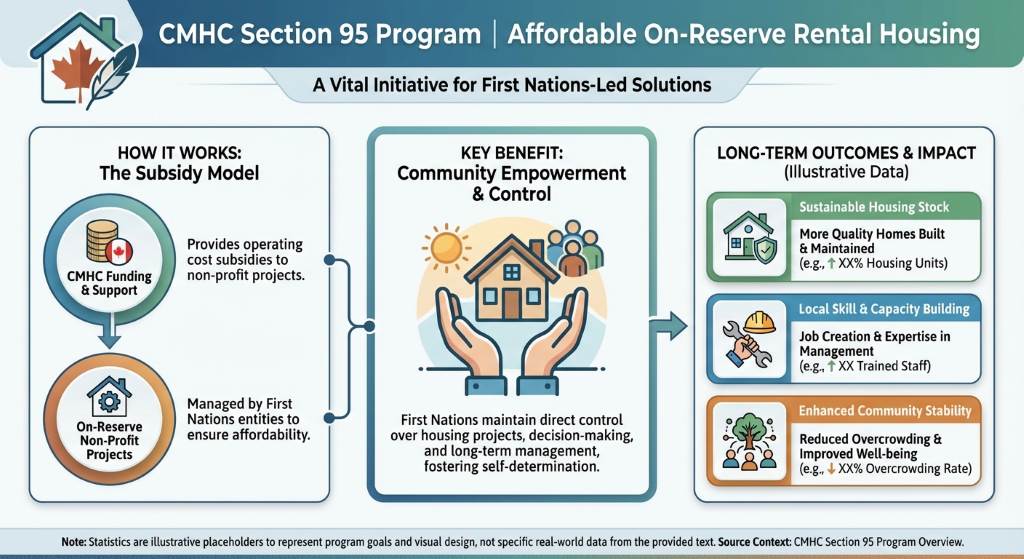

One of the most vital programs available is the CMHC Section 95 program. This initiative helps First Nations communities provide affordable rental housing to their members. Under this program, the Canada Mortgage and Housing Corporation (CMHC) provides subsidies to assist with the operating costs of on-reserve non-profit housing projects.

One of the most vital programs available is the CMHC Section 95 program. This initiative helps First Nations communities provide affordable rental housing to their members. Under this program, the Canada Mortgage and Housing Corporation (CMHC) provides subsidies to assist with the operating costs of on-reserve non-profit housing projects.

Here are the key benefits of the CMHC Section 95 and on-reserve non-profit programs:

- Community Empowerment: First Nations maintain control over the housing projects, ensuring they meet the specific needs of their members.

- Financial Support: Subsidies help bridge the gap between the cost of operating the housing and the revenue collected from rent.

- Capacity Building: Programs often include training and resources to help communities manage their housing portfolios effectively.

Securing a First Nations mortgage in Canada, especially an on-reserve loan, involves collaboration between the borrower, the First Nation council, and the lender. Because reserve lands are held in trust by the Crown, traditional mortgages do not apply. Instead, lenders rely on Ministerial Loan Guarantees (MLGs) or specialized trust arrangements. If you feel unsure about a recent bank offer, remember that we are experts at providing second opinions on Indigenous and First Nations home loans.

| Feature | Standard Canadian Mortgage | On-Reserve Loan (First Nations Mortgage) |

|---|---|---|

| Land Ownership | Fee Simple (Private Ownership) | Crown Land held in trust for the First Nation |

| Collateral | The property and the land itself | Requires a Ministerial Loan Guarantee (MLG) or Band Council Resolution |

| Lender Options | Broad range of banks, credit unions, and A-lenders | Specialized lenders participating in Indigenous Home Loans programs |

| CMHC Programs | Standard high-ratio mortgage insurance | CMHC Section 95 On-Reserve Non-Profit Housing Program |

Why Partner with an Edmonton Mortgage Broker for Your Indigenous Home Loan?

Choosing the right mortgage broker in Edmonton, AB, can make the difference between a confident purchase and unnecessary stress. Jason Scott has over 15 years of experience in the local real estate market, offering independent advice free from bank ties. We understand the nuances of first nations mortgage canada policies and are dedicated to helping Edmontonians and surrounding Indigenous communities find the best pathways to homeownership.

When you work with us, you receive:

- Unbiased Expertise: We shop over 20 lenders to find competitive options tailored to your needs.

- Personalized Strategies: From smart pre-payment privileges to debt consolidation, we build a plan to help you become mortgage-free faster.

- Local Support: Enjoy seamless pre-approvals and access to a trusted network of Edmonton realtors and inspectors.

Do not leave your homeownership dreams to chance. Let us guide you through the intricacies of Indigenous First Nations Home Loan Programs and ensure you get the best possible terms.

Q1: What is a First Nations mortgage in Canada?

A First Nations mortgage, or on-reserve loan, is a specialized financing option designed for Indigenous individuals purchasing or building homes on reserve lands, which typically require unique loan guarantees instead of traditional land collateral.

Q2: How does the CMHC Section 95 program work?

The CMHC Section 95 program provides financial assistance and subsidies to First Nations to help develop and operate affordable on-reserve non-profit rental housing for their community members.

Q3: Can I get a second opinion on an Indigenous home loan offer?

Absolutely. We are experts at providing second opinions on Indigenous and First Nations home loans, ensuring you receive the most competitive rates and fair terms available in the market.

Q4: Do I need a high-ratio insured mortgage for an off-reserve property?

If you are purchasing an off-reserve property in Edmonton or elsewhere in Alberta with a down payment of less than 20 percent, you will typically need a high-ratio insured mortgage through providers like CMHC or Sagen.

Q5: Why should I use an Edmonton mortgage broker for my on-reserve loan?

An experienced Edmonton mortgage broker like Jason Scott understands both the local Alberta market and the specific legal requirements of Indigenous Home Loans, offering unbiased advice and access to specialized lenders.

{kind=link}

{kind=link}