What is a Low-Ratio Uninsured Mortgage in Canada?

If you are exploring your home financing options in Edmonton, you have likely come across the term low-ratio uninsured mortgage. But what exactly does it mean? An uninsured mortgage in Canada is a home loan where the purchaser provides a down payment of 20 percent or more, or a homeowner has at least 20 percent equity in their property. Because you are putting down a substantial amount of your own money, the loan-to-value ratio is 80 percent or less. This means you are not required to purchase mortgage default insurance, such as CMHC insurance, which can save you thousands of dollars over the life of your loan.

A low-ratio mortgage provides exceptional flexibility for both buyers and current homeowners. Here are some of the standout benefits:

- No Costly Insurance Premiums: You completely avoid paying the typical 2.4 to 4 percent premium that gets tacked onto high-ratio insured mortgages.

- Extended Amortization Options: Uninsured mortgages can often be stretched to a 30-year amortization period, significantly lowering your monthly payments.

- Greater Property Flexibility: This mortgage type is required if you are purchasing a property valued over $1 million or buying a rental investment property.

Many borrowers choose to pair their low-ratio uninsured mortgage with a conventional-fixed-rate-mortgage for maximum stability and predictable payments. As an experienced Edmonton mortgage broker, Jason Scott and his team are experts at providing second opinions on low-ratio uninsured mortgages to ensure you secure the absolute best terms for your financial future.

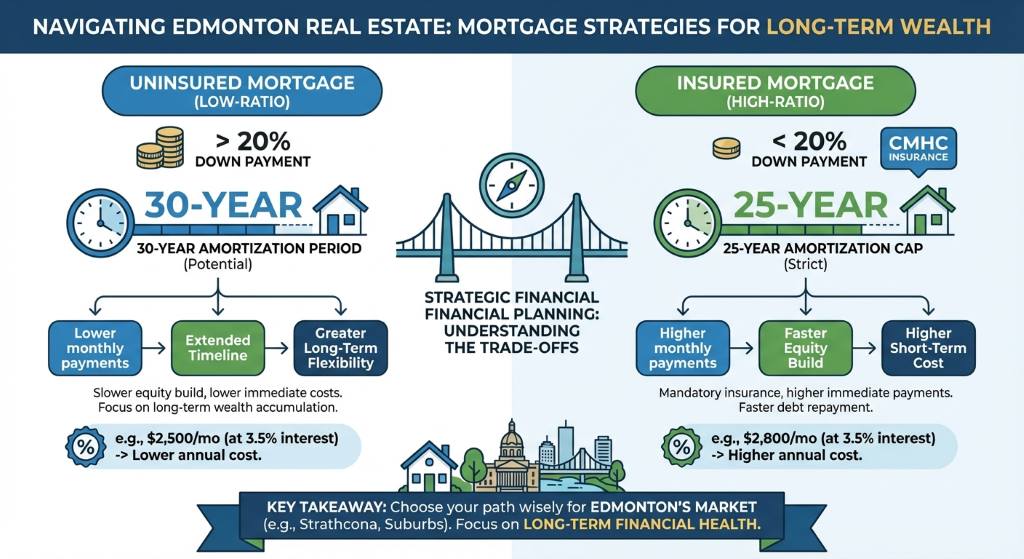

Key Differences Between Insured and Uninsured Mortgages

Navigating the Edmonton real estate market requires strategic financial planning. Whether you are looking at vibrant neighborhoods like Strathcona or upgrading to a larger family home in the suburbs, understanding how an uninsured mortgage in Canada compares to a high-ratio insured loan is vital to your long-term wealth.

Navigating the Edmonton real estate market requires strategic financial planning. Whether you are looking at vibrant neighborhoods like Strathcona or upgrading to a larger family home in the suburbs, understanding how an uninsured mortgage in Canada compares to a high-ratio insured loan is vital to your long-term wealth.

One of the biggest advantages of a low-ratio mortgage is the potential for a 30-year amortization period. While insured mortgages are strictly capped at 25 years, extending your amortization can significantly reduce your monthly cash flow burden. However, it is important to note that lenders often price uninsured mortgage rates slightly differently than insured rates. Because the lender takes on more risk without the backing of default insurance, the interest rate might vary slightly compared to an insured product.

Because rates and terms vary widely among financial institutions, we highly recommend getting a professional review of your options. Jason Scott at TMG The Mortgage Group shops over 20 different lenders to find competitive rates that consistently beat the big banks. Below is a detailed breakdown of how these two distinct mortgage types compare.

| Feature | Insured Mortgage (High-Ratio) | Uninsured Mortgage (Low-Ratio) |

|---|---|---|

| Down Payment Required | 5% to 19.99% | 20% or more |

| Mortgage Default Insurance | Mandatory (CMHC, Sagen, Canada Guaranty) | Not required |

| Maximum Amortization | 25 Years | Up to 30 Years |

| Property Value Limit | Under $1 Million | No maximum limit |

| Investment Properties | Not allowed | Allowed |

Why Get a Second Opinion on Your Low-Ratio Mortgage?

Choosing the wrong lender can cost you thousands of dollars in hidden fees, restrictive penalties, and higher interest rates. Even if your current bank has offered you a seemingly attractive rate on a low-ratio uninsured mortgage, getting an independent review is a highly recommended financial move.

Here is why thousands of Edmontonians trust Jason Scott for a second opinion:

- Unbiased Expertise: Free from big bank ties, we provide independent advice focused entirely on your unique financial goals.

- Access to Top Rates: We negotiate with dozens of lenders to secure terms tailored to your specific situation, whether you prefer a variable rate or a secure conventional-fixed-rate-mortgage.

- Long-Term Savings Strategies: We help you leverage smart pre-payment privileges so you can reach your mortgage freedom day faster without incurring unnecessary penalties.

If you are renewing, refinancing, or purchasing a new home in Edmonton with 20 percent down, let us review your paperwork. We are experts at providing second opinions on low-ratio uninsured mortgages and will ensure you are not leaving your hard-earned money on the table.

Q1: What qualifies as an uninsured mortgage in Canada?

An uninsured mortgage, also known as a low-ratio mortgage, is a home loan where the borrower has a down payment or home equity of at least 20 percent. Because the loan-to-value ratio is 80 percent or less, mortgage default insurance is not legally required.

Q2: Can I get a 30-year amortization on a low-ratio mortgage?

Yes. One of the primary benefits of a low-ratio uninsured mortgage is the ability to extend your amortization period up to 30 years. This can help significantly lower your monthly payments compared to the strict 25-year limit placed on insured mortgages.

Q3: Are interest rates higher for uninsured mortgages?

Sometimes, uninsured mortgage rates can be slightly higher than insured rates. This happens because the lender assumes more risk without the protection of default insurance. However, working with an independent Edmonton mortgage broker ensures you find the most competitive rates available across multiple lenders.

Q4: Do I need a low-ratio mortgage for an investment property in Edmonton?

Yes. If you are purchasing a rental or investment property that you will not personally occupy, Canadian regulations require a minimum 20 percent down payment. This makes it a low-ratio uninsured mortgage by default.

Q5: Why should I get a second opinion on my mortgage offer?

Bank offers are often limited strictly to their own in-house products. We are experts at providing second opinions on low-ratio uninsured mortgages. By reviewing your offer, we can often find better terms, greater flexibility, and lower rates through our extensive network of over 20 lenders.

Ready to secure the best possible terms for your home?

Contact Jason Scott for a Free ConsultationOr call us directly at (780) 721-4879

{kind=link}

{kind=link}