Understanding Foreign-Buyer and Non-Resident Mortgages in Edmonton

Navigating the real estate market from afar can feel overwhelming, but securing a non resident mortgage canada does not have to be stressful. Whether you are an investor, a frequent visitor, or someone planning to relocate to Edmonton, AB, understanding the nuances of a foreign-buyer mortgage is essential. At Edmonton Mortgage Broker, Jason Scott provides expert guidance to help non-residents and foreign buyers find the best financing options.

A non-resident mortgage allows individuals who do not live in Canada full-time to purchase property here. However, the rules, down payment requirements, and tax implications differ significantly from standard domestic loans. We specialize in comparing top lenders to secure competitive rates, ensuring you keep more money in your pocket. If you are exploring your options, we highly recommend looking into a conventional fixed-rate mortgage for stable, predictable payments.

- Unbiased Expertise: Independent advice free from bank ties.

- Local Knowledge: Deep understanding of the Edmonton real estate market.

- Second Opinions: We are experts at providing second opinions on foreign buyer and non-resident mortgages to ensure you are getting the best deal.

Visa Holder Mortgages: What You Need to Know

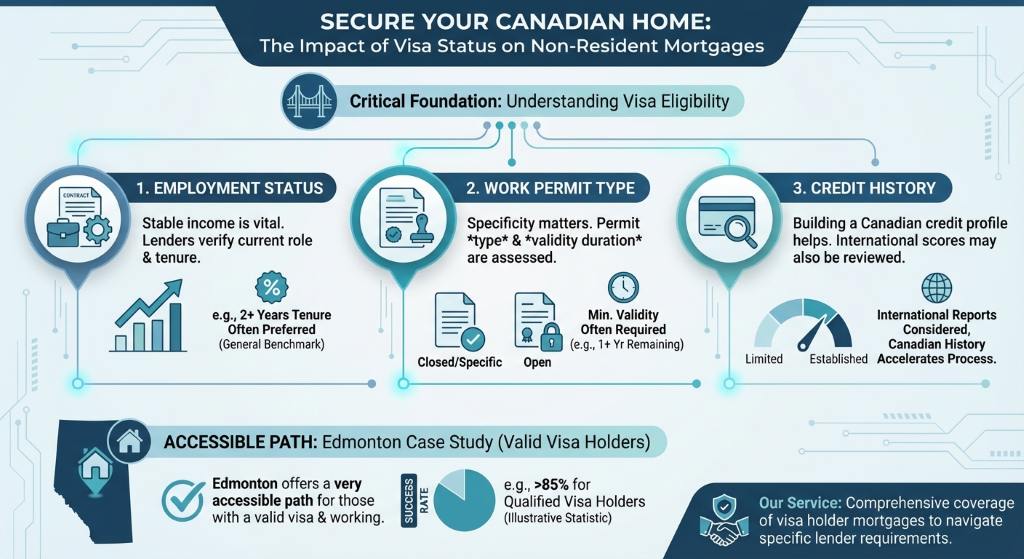

One of the most critical aspects of securing a non resident mortgage canada is understanding how visa status impacts your eligibility. Comprehensive coverage of visa holder mortgages is a key part of our service because the requirements can be highly specific. Lenders look closely at your employment status, the type of work permit you hold, and your credit history.

One of the most critical aspects of securing a non resident mortgage canada is understanding how visa status impacts your eligibility. Comprehensive coverage of visa holder mortgages is a key part of our service because the requirements can be highly specific. Lenders look closely at your employment status, the type of work permit you hold, and your credit history.

For individuals working in Edmonton on a valid visa, the path to homeownership is very accessible. Lenders typically require:

- A valid Canadian work permit.

- Proof of full-time employment.

- A letter of employment and recent pay stubs.

- A minimum down payment, which can vary based on your residency status and credit history.

If you lack a Canadian credit history, some lenders may accept international credit reports or alternative proof of creditworthiness, such as international bank reference letters. Because these policies vary wildly between lenders, working with an experienced Edmonton mortgage broker like Jason Scott is invaluable. We can help you navigate these requirements and find a lender that views your unique situation favorably.

| Applicant Type | Typical Minimum Down Payment | Credit History Requirement | Additional Documentation |

|---|---|---|---|

| Permanent Resident | 5% to 20% | Standard Canadian Credit | Standard Income Verification |

| Work Visa Holder | 5% to 10% | Canadian or Alternative Credit | Valid Work Permit, Employment Letter |

| Non-Resident / Foreign Buyer | 35% | International Credit Report | Bank Reference, Proof of Funds Source |

Why Get a Second Opinion on Your Non-Resident Mortgage?

Choosing the wrong lender can cost you thousands in hidden fees and unfavorable interest rates. This is especially true for foreign buyers who might not be familiar with the Canadian banking system. That is why we are experts at providing second opinions on foreign buyer and non-resident mortgages. If a bank has given you a quote, bring it to us. We will review the terms, compare them against over 20 different lenders, and tell you honestly if we can do better.

Edmonton is a dynamic and growing city, making it a fantastic place to invest in real estate. From navigating the complex regulations to structuring your financing correctly, Jason Scott and TMG The Mortgage Group provide the holistic support you need. We partner with vetted local professionals, including realtors and legal advisors, to ensure your transaction is seamless.

Do not settle for the first offer you receive. Let us help you explore all your options, including a reliable conventional fixed-rate mortgage, to secure your financial future in Alberta.

Q1: What is the minimum down payment for a non resident mortgage canada?

Typically, non-residents and foreign buyers are required to provide a minimum down payment of 35%. However, those on valid work visas may qualify for lower down payments, sometimes as low as 5%.

Q2: Can I get a mortgage in Edmonton if I am on a work visa?

Yes, visa holder mortgages are very common. If you have a valid Canadian work permit and proof of full-time employment, you can qualify for a mortgage with terms similar to Canadian citizens.

Q3: Do I need a Canadian credit history to buy a home in Alberta?

While a Canadian credit history is preferred, many lenders will accept an international credit report or alternative forms of credit verification, such as bank reference letters from your home country.

Q4: Are foreign buyers subject to additional taxes in Edmonton?

Unlike some other Canadian provinces, Alberta currently does not have a provincial foreign buyer tax. This makes Edmonton a highly attractive market for non-resident investors.

Q5: Why should I use a mortgage broker for a foreign-buyer mortgage?

A broker like Jason Scott has independent access to top rates from over 20 lenders. We are experts at providing second opinions on foreign buyer and non-resident mortgages, ensuring you avoid unnecessary fees and secure the best possible terms.

{kind=link}

{kind=link}