What Are Down Payment Assistance Programs?

Saving for a home in Edmonton can feel like a steep climb, but Down Payment Assistance Programs (often referred to as DPA Programs) are designed to make homeownership highly accessible. Whether you are eyeing a cozy condo in Oliver or a spacious family home in Strathcona, understanding your options for down payment assistance canada is the crucial first step to unlocking your new front door.

As your dedicated Edmonton mortgage broker, I specialize in navigating these complex offerings. DPA programs typically come in the form of provincial grants, municipal initiatives, or shared equity models. We are experts at providing second opinions on down payment assistance programs, ensuring you do not miss out on funding you actually qualify for. If you are just starting your real estate journey, exploring our first-time home buyer mortgage guide is a fantastic way to build a solid financial foundation before applying.

Exploring Provincial Grants and Forgivable Loans

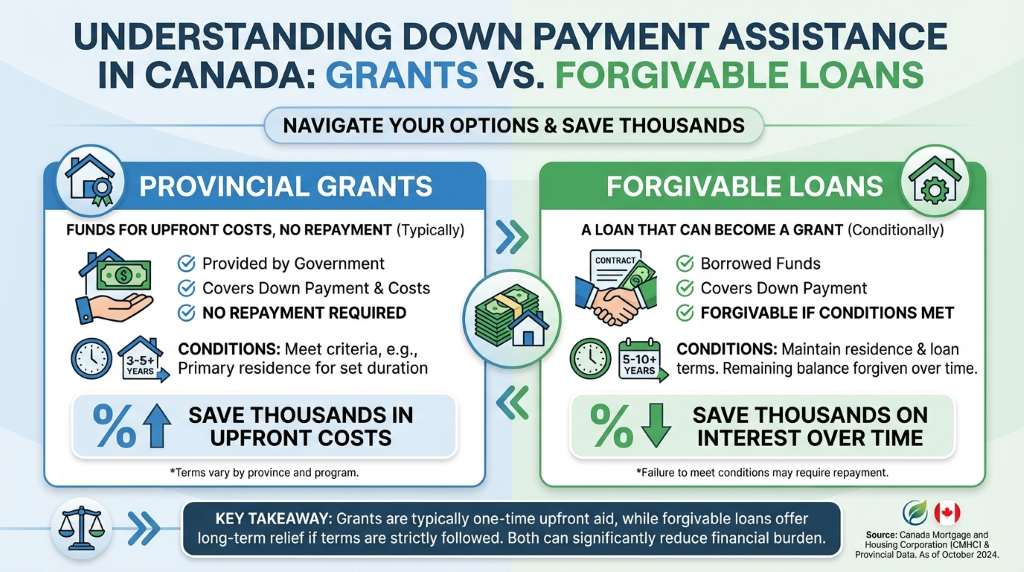

When looking into down payment assistance Canada, two of the most common structures you will encounter are provincial grants and forgivable loans. Understanding the distinction between the two can save you thousands over the life of your mortgage.

When looking into down payment assistance Canada, two of the most common structures you will encounter are provincial grants and forgivable loans. Understanding the distinction between the two can save you thousands over the life of your mortgage.

- Provincial Grants: These are funds provided by the government to help cover your upfront costs. Typically, grants do not need to be repaid as long as you meet specific criteria, such as living in the home for a set number of years.

- Forgivable Loans: A forgivable loan provides an initial lump sum for your down payment. The loan balance decreases over time and is eventually forgiven entirely, provided you maintain the property as your primary residence.

Each program has strict eligibility rules regarding household income and maximum property price. Combining these local programs with federal strategies, like the Home Buyers Plan RRSP withdrawal, can significantly reduce your upfront financial burden. Remember, choosing the wrong lender or program can be a costly mistake. Getting a professional second opinion ensures you are leveraging the right combination of provincial grants and forgivable loans for your unique financial situation.

| Program Type | Typical Assistance Amount | Repayment Terms | Best For |

|---|---|---|---|

| Provincial Grants | 3% to 5% of purchase price | No repayment required if residency terms are met | Low to moderate income buyers |

| Forgivable Loans | Up to $10,000 | Forgiven over 5 years of primary residency | First-time home buyers |

| Shared Equity Programs | 5% to 10% of purchase price | Repaid upon sale based on current home value | Buyers needing lower monthly payments |

How an Edmonton Mortgage Broker Can Help You Qualify

In Edmonton’s dynamic real estate market, securing the right mortgage and maximizing your down payment assistance requires unbiased expertise. As an independent broker with over 15 years in the YEG market, I shop over 20 lenders to find competitive options that often beat the standard big bank offers.

We know that navigating the paperwork for a forgivable loan or a provincial grant can feel overwhelming. That is exactly why our education-first approach simplifies the process. We will review your finances, help you understand high-ratio mortgages, and determine exactly which DPA programs you qualify for. If you have already been denied or given a generic offer by your bank, reach out to us. We are experts at providing second opinions on down payment assistance programs, and we pride ourselves on building personalized strategies that save Edmontonians thousands of dollars.

Q1: What is down payment assistance in Canada?

Down payment assistance in Canada includes various provincial grants, forgivable loans, and shared equity programs designed to help eligible buyers cover the upfront costs of purchasing a home.

Q2: Do I have to pay back a forgivable loan?

Generally, no. As long as you meet the specific conditions of the program, such as living in the home as your primary residence for a set period of time, the loan is completely forgiven.

Q3: Can I combine DPA programs with the Home Buyers Plan?

Yes, many buyers successfully combine provincial down payment assistance with the federal Home Buyers Plan, allowing them to withdraw funds from their RRSP tax-free to boost their total down payment.

Q4: What is the minimum down payment for a home in Edmonton?

For homes under $500,000, the minimum down payment is 5%. Programs like grants or forgivable loans can help you reach this 5% threshold without completely draining your savings.

Q5: Why should I get a second opinion on my mortgage application?

Bank advisors only offer their own specific products. An independent Edmonton mortgage broker can review your file, explore over 20 different lenders, and ensure you are not missing out on hidden grants or better interest rates.

Contact Jason Scott Today for a Free Down Payment Assistance Consultation

{kind=link}

{kind=link}