Understanding Vacation Cottage-Property Mortgages

Owning a peaceful getaway is a lifelong dream for many Albertans. Whether you are searching for a summer retreat or a year-round cabin in the woods, understanding the intricacies of a Vacation Cottage-Property Mortgage is your first crucial step. Often referred to simply as a Cottage Mortgage, this type of financing differs significantly from a standard residential home loan.

When exploring a cottage mortgage canada, it is important to know that lenders evaluate these properties based on their accessibility, winterization, and location. Because these are not primary residences, the lending criteria can sometimes be stricter. However, with the right guidance from an experienced Edmonton mortgage broker, securing the keys to your dream property is entirely achievable.

- Unique Lending Criteria: Lenders assess the property’s foundation, heating source, and year-round road access.

- Down Payment Variations: Depending on the property type, your required down payment could range from 5% to 20%.

- Cross-Border Comparisons: If you are looking outside of Canada, the rules change entirely. For instance, you might want to explore how a second-home-vacation-home-mortgage USA operates compared to domestic options.

At Jason Scott, TMG The Mortgage Group, we specialize in helping Edmontonians navigate these unique financial waters. We are experts at providing second opinions on vacation and cottage property mortgages to ensure you are getting the most competitive rate possible.

Financing Waterfront Cottages and Seasonal Property Loans

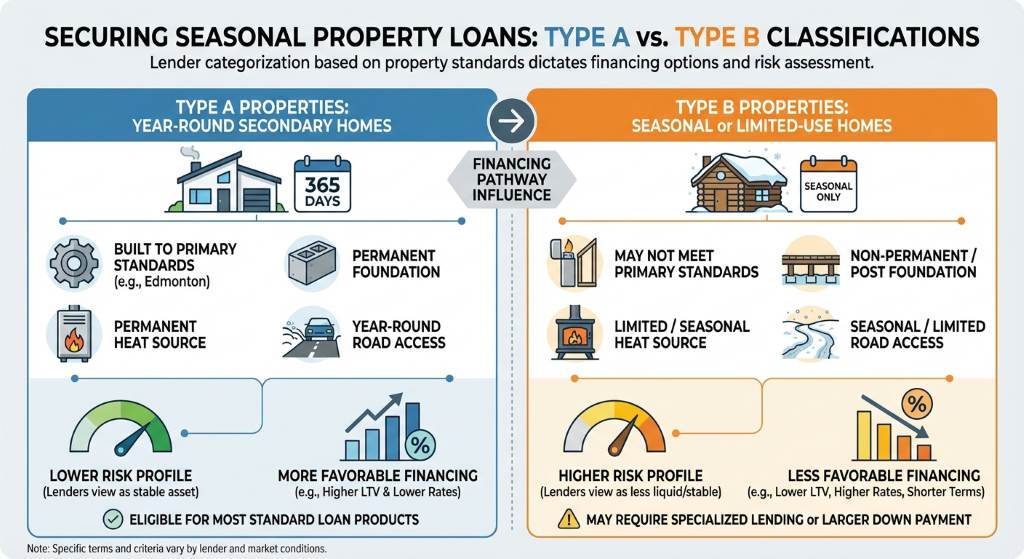

When it comes to securing seasonal property loans, lenders typically categorize properties into two main groups: Type A and Type B. Understanding which category your desired property falls into will dictate your financing options.

When it comes to securing seasonal property loans, lenders typically categorize properties into two main groups: Type A and Type B. Understanding which category your desired property falls into will dictate your financing options.

Type A Properties (Year-Round Secondary Homes): These properties are built to the same standards as your primary residence in Edmonton. They feature a permanent foundation, a permanent heat source, and year-round road access. Because they are considered less risky, you can often secure a mortgage for these waterfront cottages with as little as a 5% down payment.

Type B Properties (Seasonal Cottages): These are un-winterized properties that might lack a permanent heat source or year-round road access. Think of a rustic summer cabin accessible only by boat or unplowed roads in the winter. For these seasonal property loans, lenders generally require a minimum 10% down payment, and the maximum loan amount may be capped.

Working with an independent broker like Jason Scott means you get unbiased expertise. We shop over 20 lenders to find the perfect fit for your specific property type, ensuring you do not overpay on interest or accept restrictive terms.

| Property Characteristic | Type A (Year-Round) | Type B (Seasonal) |

|---|---|---|

| Winterization | Fully winterized with permanent heat | Un-winterized or seasonal heat only |

| Foundation | Permanent foundation | Floating, blocks, or non-permanent |

| Access | Year-round, municipally maintained road | Seasonal road or boat access only |

| Minimum Down Payment | 5% (with default insurance) | 10% (with default insurance) |

| Lender Availability | Widely accepted by most major lenders | Restricted to select specialized lenders |

Why You Need a Second Opinion on Your Vacation Cottage-Property Mortgage

In Edmonton’s dynamic real estate market, choosing the right mortgage broker means the difference between a confident purchase and unnecessary stress. If you have already received a quote from your primary bank for a cottage property, do not sign on the dotted line just yet.

We are experts at providing second opinions on vacation and cottage property mortgages. Banks often have rigid guidelines regarding rural properties, well water testing, and septic systems. An independent broker has access to specialized lenders who are much more flexible with seasonal property loans and waterfront cottages. A second opinion can uncover:

- Lower Interest Rates: We often beat bank offers by leveraging our network of 20+ lenders.

- Better Pre-Payment Privileges: Pay off your cottage faster without facing harsh penalties.

- Flexible Equity Options: We can help you leverage the equity in your current Edmonton home to fund your new vacation property.

Let us do the heavy lifting. A quick review of your current pre-approval could save you thousands of dollars over the life of your term.

Q1: What is the minimum down payment for a cottage mortgage in Canada?

For a fully winterized, year-round property (Type A), the minimum down payment is 5%. For a seasonal, un-winterized property (Type B), you will need a minimum down payment of 10%.

Q2: Can I use the equity in my Edmonton home to buy a waterfront cottage?

Absolutely. Many homeowners choose to refinance their primary residence or use a Home Equity Line of Credit (HELOC) to secure the down payment or purchase a vacation property outright.

Q3: Are interest rates higher for seasonal property loans?

Interest rates for vacation properties are typically very competitive and often mirror primary residence rates, especially for Type A properties. Type B properties might carry a slight premium depending on the lender.

Q4: What qualifies as a waterfront cottage for mortgage purposes?

Lenders look at factors like the property’s foundation, water source (well or lake intake), septic system, and road access. A property must meet specific health and safety standards to qualify for standard financing.

Q5: Why should I get a second opinion on my vacation cottage-property mortgage?

Different lenders have vastly different rules for rural and seasonal properties. A second opinion from an expert broker ensures you are not being denied unnecessarily or overpaying on interest due to a bank’s restrictive rural lending policies.

{kind=link}

{kind=link}