Is 2026 the Right Year to Refinance Your Edmonton Home?

Welcome to 2026. If you have been holding your breath through the volatility of the last few years, you aren’t alone. Fortunately, the financial landscape in Edmonton is shifting. With the Bank of Canada holding rates steady and lenders offering more competitive products, we are finally seeing a “sweet spot” for homeowners.

As your dedicated Edmonton mortgage broker, I’ve seen firsthand how stabilizing rates are opening doors for smart financial moves. Refinancing isn’t just about getting a lower interest rate; it is a strategic tool to access equity, consolidate high-interest debt, or fund renovations to increase your property value. Whether you are in Strathcona, Oliver, or the suburbs, understanding the refinancing rules and opportunities in 2026 is key to mastering your cash flow.

Top Strategic Reasons to Refinance Now

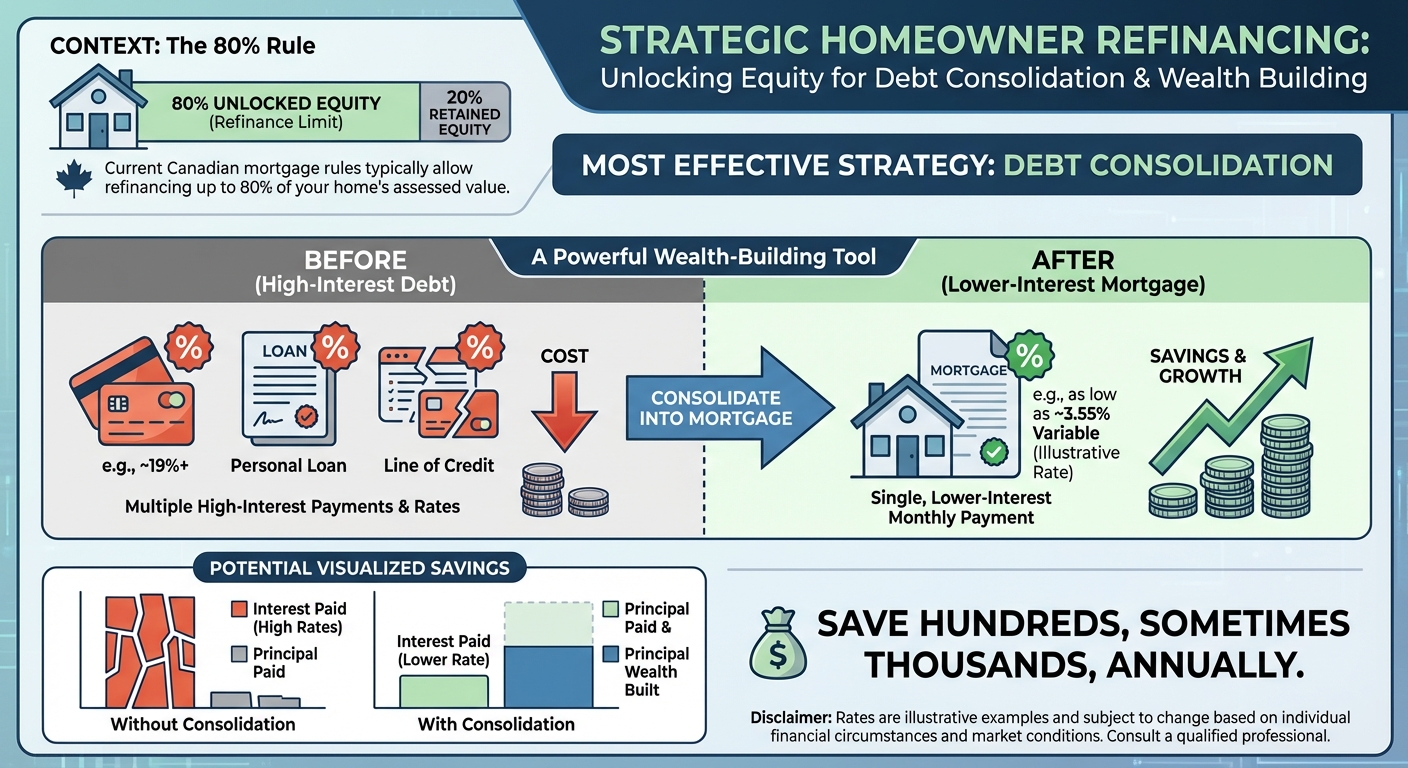

Many homeowners typically refinance to borrow equity for specific life goals. Under current Canadian mortgage rules, you can refinance up to 80% of your home’s value. Here are the most effective strategies we are seeing clients use this year:

- Debt Consolidation: This is the most powerful wealth-building tool available. By rolling high-interest credit card debt (often 19%+) or personal lines of credit into your mortgage (at rates as low as 3.55% variable), you can save hundreds, sometimes thousands, in monthly cash flow.

- Home Renovations: With Edmonton’s housing market remaining active, using equity to finish a basement or upgrade a kitchen can significantly increase your resale value.

- Investment Properties: Savvy investors are pulling equity to fund down payments for rental properties while the market is balanced.

At Jason Scott – TMG The Mortgage Group, we analyze your specific situation to ensure the long-term savings outweigh the costs of breaking your current term.

| Mortgage Term | Big Bank Posted Rate | Our Best Rates (Jason Scott) | Potential Savings |

|---|---|---|---|

| 5-Year Variable | 4.45% | 3.55% | 0.90% lower rate |

| 5-Year Fixed | 6.09% | 3.89% | 2.20% lower rate |

| 3-Year Fixed | 6.05% | 3.99% | 2.06% lower rate |

*Rates subject to change. Based on 2026 market data.

Calculating the Cost: Penalties vs. Savings

One of the biggest hesitations homeowners have is the penalty for breaking a mortgage early. This is where unbiased advice is critical. Lenders typically charge the greater of three months’ interest or the Interest Rate Differential (IRD). While the IRD can sometimes be expensive with big banks, the math often still works in your favor.

For example, if paying a $3,000 penalty saves you $400 a month in interest payments via debt consolidation, you recoup that cost in less than a year. The rest of the term is pure savings. I calculate this “break-even point” for every client so you can make a confident decision without the guesswork.

Q1: What is the maximum amount I can refinance from my home in Edmonton?

In Canada, you can refinance up to 80% of the appraised value of your home, minus your remaining mortgage balance.

Q2: Does refinancing hurt my credit score?

There is a minor, temporary dip due to the credit inquiry, but using the funds to pay off high-utilization credit cards usually improves your score significantly in the long run.

Q3: Should I choose a fixed or variable rate when refinancing in 2026?

It depends on your risk tolerance. Currently, our variable rates (approx. 3.55%) are lower than fixed, but fixed offers stability if you prefer consistent payments.

Q4: What costs are involved in refinancing?

Expect to budget for a mortgage discharge fee, legal fees, and an appraisal fee. However, these can often be rolled into the new mortgage amount.

Q5: How long does the refinance process take?

With a broker, the process is streamlined. Once we have your documents, it typically takes 2 to 3 weeks to fund.

{kind=link}

{kind=link}